Table of Contents

Stata is a sophisticated integrated statistical software package that provides researchers, economists, and data scientists with a robust suite of tools for data management, visualization, and advanced econometric modeling. One of the most fundamental tasks in exploratory data analysis is determining the underlying distribution of a dataset. Specifically, identifying whether a variable follows a normal distribution is essential because many classical statistical procedures—including t-tests, ANOVA, and linear regression—rely on the assumption of normality to produce valid p-values and confidence intervals. When data deviates significantly from this “bell-shaped” curve, the reliability of these parametric tests may be compromised, leading to potentially erroneous conclusions.

In the Stata environment, users have access to a diverse array of methodologies to evaluate normality, ranging from intuitive graphical inspections to rigorous statistical hypothesis testing. Graphical methods, such as histograms and Q-Q plots, offer a visual representation of the data’s spread, allowing researchers to spot outliers or skewness immediately. On the other hand, formal tests provide a definitive p-value that quantifies the evidence against the null hypothesis of normality. By combining these approaches, analysts can make informed decisions regarding whether to proceed with parametric methods or to employ non-parametric alternatives and data transformations.

This comprehensive guide explores the primary techniques available in Stata for testing normality. We will examine the practical application of histograms, the Shapiro-Wilk test, the Shapiro-Francia test, and the Skewness and Kurtosis test. Each method has specific requirements regarding sample size and sensitivity to different types of distributional deviations. Understanding these nuances is critical for any researcher aiming to maintain high standards of statistical integrity in their empirical work.

The Theoretical Importance of the Normal Distribution

The normal distribution, often referred to as the Gaussian distribution, serves as the cornerstone of inferential statistics. This importance stems largely from the Central Limit Theorem, which posits that the distribution of the sample mean tends toward normality as the sample size increases, regardless of the population’s original distribution. However, for smaller samples, the assumption that the data itself is normally distributed remains vital for the validity of parametric statistics. If a variable is non-normal, the standard errors of estimates may be biased, which directly impacts the statistical significance of the results.

Beyond simple significance testing, normality is a key assumption in the analysis of residuals in regression analysis. For a linear regression model to be considered the Best Linear Unbiased Estimator (BLUE), the errors should ideally be independent and identically distributed (i.i.d.) following a normal distribution. While Ordinary Least Squares (OLS) regression is somewhat robust to violations of this assumption in large samples, extreme skewness or heavy tails (kurtosis) can significantly distort the predictive power and accuracy of the model. Therefore, testing for normality is not merely a box-ticking exercise but a foundational step in ensuring model specification is correct.

Researchers must also distinguish between the normality of the raw data and the normality of the error terms. In many instances, independent variables do not need to be normally distributed; however, the dependent variable’s relationship with these predictors should result in normally distributed residuals. By mastering the normality tests within Stata, analysts can determine if their data requires a logarithmic transformation, a Box-Cox transformation, or if they should switch to a generalized linear model (GLM) that accommodates different error structures.

Initial Setup and Loading the Dataset in Stata

Before implementing any diagnostic tests, it is necessary to prepare the Stata workspace and load an appropriate dataset. For the purposes of this tutorial, we will utilize the auto dataset, which is a classic built-in Stata dataset containing various attributes of 1978 automobiles. This dataset is ideal for demonstrating normality tests because it contains variables with different distributional characteristics, such as weight, mileage (mpg), and engine displacement. Accessing this data is straightforward and requires only a single command in the Stata Command window.

To begin, clear any existing data in the memory to avoid conflicts and then load the system dataset. This ensures that the environment is “clean” and that the variables we reference are exactly as expected. The following command retrieves the dataset from the Stata system directory and makes it active for analysis:

sysuse auto

Once the dataset is loaded, it is good practice to use the describe and summarize commands to get a preliminary overview of the variables. The displacement variable, which measures engine size, is particularly interesting for normality testing because it often exhibits skewness in automotive data. By examining the mean, standard deviation, minimum, and maximum values, we can begin to form an intuition about the data’s shape before applying more formal tests. This initial phase of data cleaning and exploration is a prerequisite for any meaningful statistical analysis.

Method 1: Visual Inspection Using Histograms

The most intuitive way to assess the distribution of a variable is through graphical visualization. A histogram partitions the data into discrete intervals (bins) and displays the frequency of observations within each bin. In a normal distribution, the histogram should be symmetric and bell-shaped, with the highest frequency of data points clustered around the mean and fewer observations appearing in the “tails” of the distribution. Any significant deviation, such as a long tail to the right or left, indicates a lack of normality.

To generate a basic histogram for the displacement variable in Stata, we utilize the hist command. This command is highly customizable, allowing users to adjust bin widths or display percentages instead of raw frequencies. For our initial assessment, we run the following:

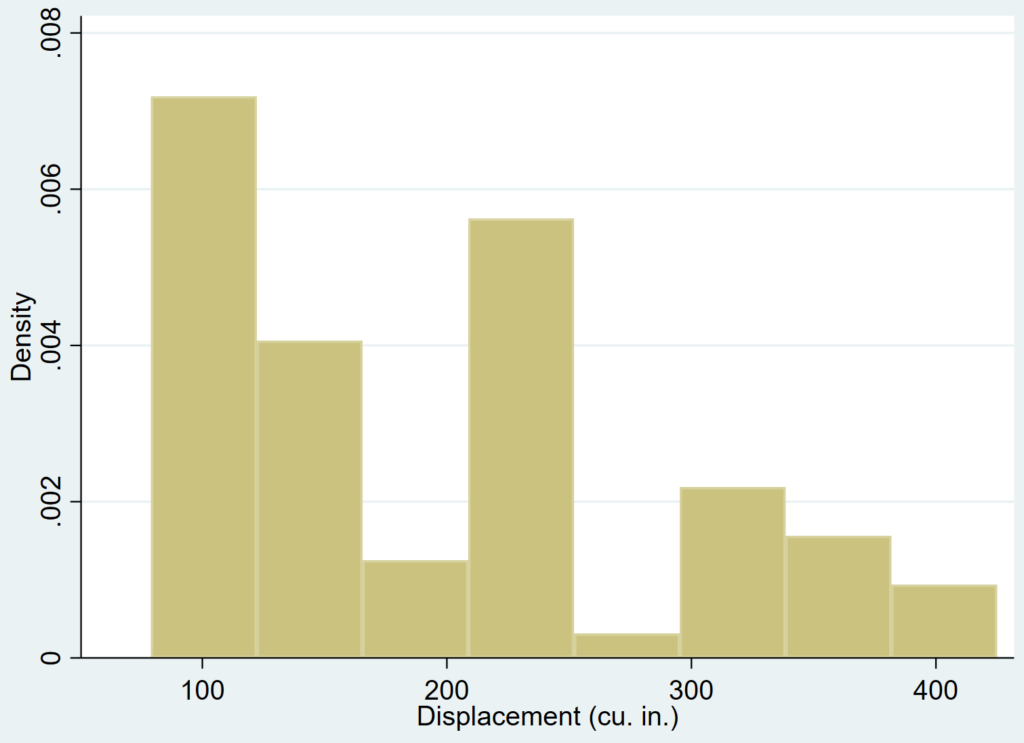

hist displacement

While a standard histogram provides a general sense of the data’s shape, it can be difficult to judge normality without a reference line. Stata allows for the overlay of a theoretical normal density curve onto the histogram. This curve represents what the distribution would look like if it perfectly followed a Gaussian model with the same mean and standard deviation as your sample. Adding this curve makes it much easier to identify skewness or kurtosis. Execute the following command to see this comparison:

hist displacement, normal

Upon reviewing the output, it becomes evident that the displacement variable is not normally distributed. The data is positively skewed (right-skewed), as characterized by the cluster of values on the left side of the graph and a long tail extending toward the higher values on the right. While graphical methods are excellent for a quick “sanity check,” they are subjective. Different bin sizes can change the appearance of the histogram, potentially leading to different interpretations. Consequently, formal statistical hypothesis testing is required to confirm these visual findings.

Method 2: The Shapiro-Wilk Test for Normality

The Shapiro-Wilk test is widely regarded as one of the most powerful and reliable formal tests for normality, particularly for small to moderate sample sizes. The null hypothesis (H0) for the test is that the sample data is drawn from a normally distributed population. If the p-value generated by the test is below a chosen significance level (commonly 0.05), we reject the null hypothesis and conclude that the data is not normally distributed. In Stata, this test is implemented using the swilk command, which is restricted to datasets containing between 4 and 2,000 observations.

To perform the Shapiro-Wilk test on the displacement variable, input the following command into the Stata console:

swilk displacement

The output provides several key metrics that require careful interpretation. The Obs column shows that 74 observations were analyzed. The W statistic is the actual Shapiro-Wilk test statistic; values closer to 1.0 suggest normality. Most importantly, the Prob > z value represents the p-value. In this case, the p-value is approximately 0.00031. Since this value is significantly less than the 0.05 threshold, we have strong evidence to reject the assumption of normality for displacement.

One of the advantages of the swilk command is its ability to process multiple variables simultaneously. This is highly efficient when dealing with large datasets where several variables need to be checked before running a multivariate analysis. For example, to test displacement, mpg, and length in one go, use the following syntax:

swilk displacement mpg length

In this multi-variable output, we observe that both displacement and mpg have p-values below 0.05, indicating non-normality. However, the length variable returns a p-value greater than 0.05. Therefore, for length, we fail to reject the null hypothesis, suggesting that its distribution does not significantly deviate from a normal distribution at the 5% significance level. This highlights how different variables within the same dataset can exhibit vastly different distributional properties.

Method 3: The Shapiro-Francia Test for Larger Samples

While the Shapiro-Wilk test is excellent, it has sample size limitations. The Shapiro-Francia test is an alternative that functions similarly but is designed to handle slightly larger datasets, specifically those with between 10 and 5,000 observations. It is essentially a modification of the Shapiro-Wilk procedure that simplifies the calculation of the test statistic, making it computationally efficient for larger N. Like its counterpart, the Shapiro-Francia test operates under the null hypothesis that the variable is normally distributed.

To execute this test in Stata, we use the sfrancia command. This is particularly useful when you have passed the 2,000-observation limit of swilk but still want a test based on the correlation between ordered observations and expected normal quantiles. To test the displacement variable, use:

sfrancia displacement

The interpretation of the Shapiro-Francia output mirrors that of the Shapiro-Wilk. In the results, the W’ (W-prime) statistic serves as the test metric, and the Prob > z provides the p-value. For our displacement data, the p-value is 0.00094. Again, because this is well below 0.05, we conclude that the variable is not normally distributed. The consistency between the Shapiro-Wilk and Shapiro-Francia tests in this instance reinforces our conclusion regarding the data’s non-normality.

It is important to note that as sample sizes become very large, almost any formal test will detect even trivial deviations from normality, leading to a rejected null hypothesis. This is a known phenomenon in statistical hypothesis testing where the test becomes “overpowered.” In such cases, the Shapiro-Francia test remains a useful tool, but researchers should weigh the statistical significance against the practical significance by also consulting graphical plots. Efficiency and robustness make sfrancia a staple in the Stata user’s toolkit for econometric analysis.

Method 4: The Skewness and Kurtosis Test (D’Agostino’s K-squared)

Another powerful alternative in Stata is the Skewness and Kurtosis test, often accessed via the sktest command. This test is based on D’Agostino’s K-squared test and evaluates normality by examining the skewness (asymmetry) and kurtosis (peakedness/heaviness of tails) of the data. A perfectly normal distribution has a skewness of 0 and a kurtosis of 3. The sktest calculates how much the sample’s values deviate from these ideals and combines them into an aggregate chi-squared test statistic. This test requires a minimum of 8 observations to run effectively.

To run the Skewness and Kurtosis test for the displacement variable, enter the following:

sktest displacement

The interpretation of sktest is slightly different as it provides individual p-values for skewness and kurtosis, followed by a combined probability. In our output, the adj chi2(2) is 5.81, and the Prob > chi2 (the overall p-value) is 0.0547. Interestingly, at a strict 0.05 significance level, this test fails to reject the null hypothesis, as 0.0547 is slightly higher than 0.05. This result contrasts with the Shapiro-Wilk and Shapiro-Francia tests, illustrating how different statistical tests can yield varying results based on the specific characteristics of the data they emphasize.

The discrepancy observed here is a perfect example of why researchers should not rely on a single test. The sktest focuses on the third and fourth moments of the distribution, while the Shapiro-Wilk test is based on the correlation between the data and normal scores. When tests disagree, it usually suggests that the deviation from normality is subtle or specific to one aspect of the distribution (like the tails). Just like the other commands, sktest can be applied to multiple variables at once, providing a rapid way to check the symmetry and tail-heaviness of your entire dataset.

Choosing the Right Test and Interpreting Discrepancies

With multiple methods available in Stata, the question arises: which test should you trust? Generally, the Shapiro-Wilk test is preferred for its high statistical power, especially in smaller samples. However, the Skewness and Kurtosis test (sktest) provides valuable insight into why a distribution might be non-normal. For instance, if the p-value for skewness is low but the kurtosis p-value is high, you know the primary issue is asymmetry rather than extreme outliers. This distinction is crucial when deciding on a data transformation strategy.

Discrepancies between tests, as seen with our displacement variable where swilk rejected normality but sktest barely did not, often occur near the “borderline” of significance. In these situations, the visual evidence from histograms or Normal Probability Plots (P-P plots) should act as the tie-breaker. If the histogram shows a clear and significant lean, as it did for displacement, it is safer to treat the data as non-normal despite a borderline p-value from a specific test. Statistical analysis is as much an art as it is a science, requiring balanced judgment between formal output and visual patterns.

Furthermore, sample size plays a pivotal role in test selection. In very small samples (N < 20), normality tests often lack the power to detect even significant non-normality. Conversely, in very large samples, even a minuscule and irrelevant deviation from a normal distribution will result in a statistically significant p-value. Therefore, for large datasets, many statisticians prioritize graphical methods and the Central Limit Theorem over formal tests. Understanding these limitations ensures that the researcher does not overreact to p-values that may not have practical implications for the robustness of their final model.

Practical Steps for Handling Non-Normal Data

Once you have determined that your data is non-normal, the next step is deciding how to handle it. One common approach in Stata is data transformation. Applying a logarithmic transformation (gen log_var = log(original_var)) can often correct positive skewness, making the distribution more symmetric and closer to normal. Other options include the square root transformation for count data or the inverse transformation for extreme skewness. After transforming the data, it is essential to re-run the normality tests to verify that the transformation was successful.

If transformations fail to achieve normality, or if the research question requires the original scale of the variable, non-parametric tests may be the best alternative. These tests, such as the Mann-Whitney U test or the Kruskal-Wallis test, do not assume a specific underlying distribution and are based on the ranks of the data rather than the raw values. Stata has comprehensive support for these methods, which provide a valid way to conduct hypothesis testing without the stringent requirements of parametric statistics.

Finally, researchers may choose to use robust standard errors or bootstrapping techniques. Bootstrapping involves repeatedly resampling the data to estimate the sampling distribution of a statistic empirically, rather than relying on theoretical assumptions. This is particularly useful in regression analysis when residuals are non-normal. By using Stata’s vce(robust) or bootstrap options, you can obtain valid inference even when the assumption of normality is violated. Ultimately, the goal is to ensure that the statistical conclusions are reliable and replicable, regardless of the initial shape of the data distribution.

Cite this article

stats writer (2026). How to Test for Normality in Stata: A Step-by-Step Guide. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/is-there-a-way-to-test-for-normality-in-stata/

stats writer. "How to Test for Normality in Stata: A Step-by-Step Guide." PSYCHOLOGICAL SCALES, 9 Mar. 2026, https://scales.arabpsychology.com/stats/is-there-a-way-to-test-for-normality-in-stata/.

stats writer. "How to Test for Normality in Stata: A Step-by-Step Guide." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/is-there-a-way-to-test-for-normality-in-stata/.

stats writer (2026) 'How to Test for Normality in Stata: A Step-by-Step Guide', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/is-there-a-way-to-test-for-normality-in-stata/.

[1] stats writer, "How to Test for Normality in Stata: A Step-by-Step Guide," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Test for Normality in Stata: A Step-by-Step Guide. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.