Table of Contents

Calculating compound interest on a daily basis is one of the most powerful tools available to investors, demonstrating how even small returns can rapidly accelerate growth over time. Using Excel allows for precise modeling and forecasting of these returns, providing a clear visualization of financial accrual. Unlike simple interest, which is calculated only on the initial investment amount, compound interest is earned on both the initial principal and the accumulated interest from previous periods. When compounding occurs daily, this effect is maximized, as interest is added back into the principal 365 times per year, creating continuous growth momentum.

To accurately perform this calculation in Excel, we primarily rely on the foundational mathematical formula for compound interest, although professional users often utilize built-in financial functions like the Future Value (FV) function for efficiency. Understanding the underlying formula is crucial, as it forces the user to correctly adjust the annual interest rate and the number of periods to account for the daily compounding frequency. This transformation—dividing the annual rate by 365 and multiplying the number of years by 365—is the critical step in moving from annual compounding to daily compounding within the spreadsheet environment, ensuring the model reflects real-world growth patterns accurately.

This guide provides a comprehensive breakdown of how to structure your data, apply the correct mathematical formulas, and interpret the results in Excel, enabling you to calculate the final value of any daily compounded investment precisely. We will explore both the manual formula input method and the more streamlined approach using Excel’s dedicated financial tools, ensuring you have robust methods for analyzing investment growth over short and long time horizons.

The Core Mathematical Formula for Compounding

The standard formula for calculating the ending value of an investment after a specific duration, considering compounding, is fundamental to financial modeling. This equation ensures that the impact of compounding frequency is accurately captured, providing the true Future Value (FV) of the investment. It is essential to master this equation before transitioning to Excel functions, as it clarifies the relationship between the various financial variables.

We utilize the following formula to determine the ending value of an investment after a certain amount of time:

A = P(1 + r/n)nt

Where each variable represents a specific component of the investment structure:

- A: The Future Value or Final Amount accumulated after t years.

- P: The Initial Principal amount invested.

- r: The nominal Annual Interest Rate, expressed as a decimal (e.g., 6% is 0.06).

- n: The Number of compounding periods per year.

- t: The Total number of years the money is invested.

When dealing specifically with daily compounding, the number of compounding periods per year (n) must be set to 365 (assuming a non-leap year). This is the key modification that ensures the interest rate is applied and reinvested on a daily cycle. By incorporating 365 into the formula, we transform an annually based calculation into a highly frequent daily model, maximizing the exponential growth potential of the investment.

If the investment is compounded daily, then we substitute 365 for n in the original equation:

A = P(1 + r/365)365t

The following example demonstrates precisely how to implement this fundamental formula within Excel to calculate the final accumulated value of an investment that benefits from daily compounding over a defined term.

Preparing Your Data in Microsoft Excel

Before applying any formulas, it is best practice to organize the input variables clearly within your Excel worksheet. This organization improves readability, facilitates auditing, and allows for easy adjustment of variables without needing to edit the formulas themselves. Start by setting up distinct cells for the principal, the annual interest rate, the compounding frequency, and the time horizon.

For our primary example, let us assume we are investing $5,000 into an account. The investment provides a nominal annual return rate of 6% and, crucially, compounds on a daily basis. We want to project the value of this investment after a period of 10 years. We must input these parameters into separate, clearly labeled cells. For instance, Cell A1 could hold “$5,000” (Principal), Cell B1 could hold “6%” (Annual Rate), and Cell C1 could hold “10” (Years).

When inputting the annual interest rate (r), remember that Excel handles percentage formatting automatically, but when used in the formula, it must be divided by the compounding frequency (n). Ensure your rate cell is formatted as a percentage or input as a decimal (0.06). The explicit definition of the compounding periods (n=365) is also a variable that should be available, often placed in a dedicated cell, which we will reference throughout our calculations to maintain consistency and flexibility across different compounding frequencies (e.g., monthly, quarterly, or daily).

Method 1: Calculating Total Value Using the Compound Interest Formula

This method involves directly translating the derived mathematical formula, A = P(1 + r/365)365t, into an Excel cell formula. This approach is highly transparent, allowing users to see exactly how each financial variable contributes to the final outcome. We will use cell referencing to make the calculation dynamic.

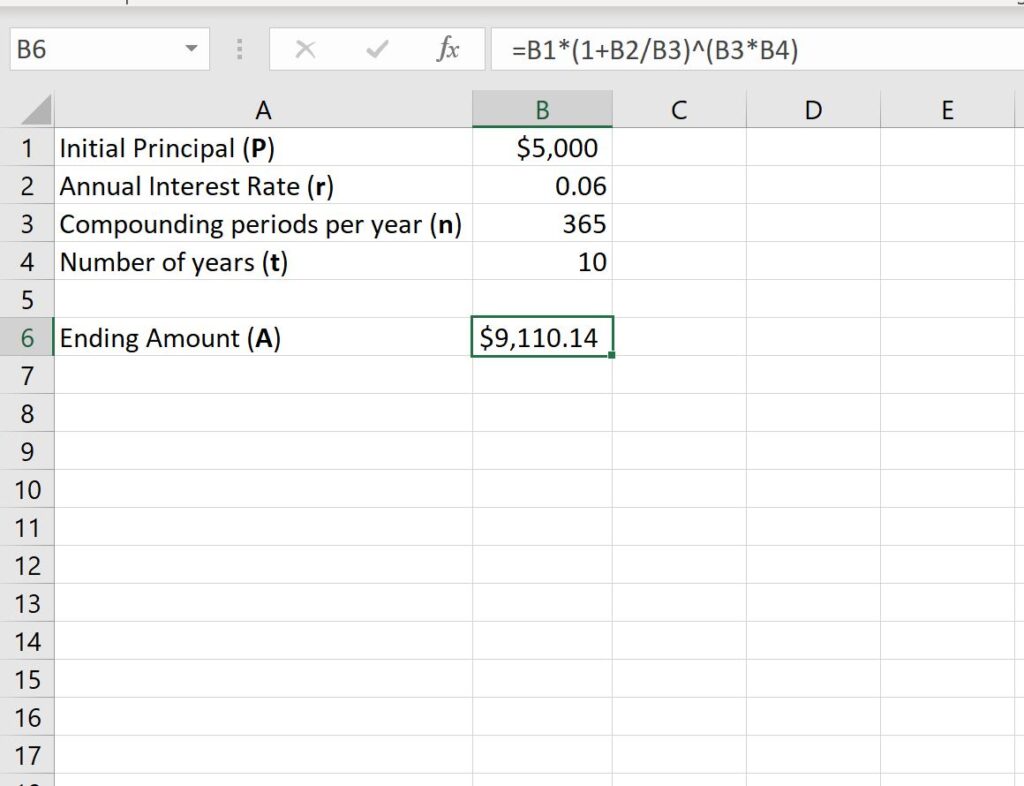

Suppose your initial principal ($5,000) is in cell B2, the annual rate (6%) is in cell B3, and the term in years (10) is in cell B4. The calculation for the final amount (A) would be entered into a separate cell, say B6. The formula structure must correctly handle the exponentiation required by the compounding logic. This involves raising the term (1 + r/365) to the power of the total number of compounding periods (365 * t).

The following screenshot illustrates how to set up the data and input the necessary formula in Excel to calculate the ending value of this daily compounded investment after 10 years. Note the direct translation of the variables into cell references within the formula structure:

The resulting calculation shows that this investment will be worth exactly $9,110.14 after the 10-year period, reflecting the consistent growth driven by daily reinvestment. This value represents the total accumulated amount, including both the initial principal and the total generated compound interest.

Method 2: Utilizing the Future Value (FV) Function

While the direct formula input works perfectly, Excel provides a cleaner, dedicated solution for calculating the final value of a stream of cash flows or a lump-sum investment: the FV function. The syntax for the FV function is: =FV(rate, nper, pmt, [pv], [type]). When calculating the growth of a single lump sum (like our $5,000 principal) without periodic payments, we must correctly define the first four arguments.

The critical requirement when using the FV function for daily compounding is the correct scaling of the rate and nper arguments. Since the function expects the rate and period to match the compounding frequency, we must adjust the annual rate (B3) and the total years (B4) accordingly. The rate argument must be the daily rate (Annual Rate / 365), and nper (Number of Periods) must be the total number of days (Years * 365).

The pmt (Payment) argument should be 0, as we are modeling a single lump sum, not an annuity. The pv (Present Value) argument is the initial principal, which must be entered as a negative value in financial functions to indicate an outflow of cash (e.g., -B2). If the principal is not entered as a negative, the result will be negative, though numerically correct. Assuming the Principal is in B2, the Rate is in B3, and the Years are in B4, the final formula using the FV function would be: =FV(B3/365, B4*365, 0, -B2). This provides the exact same result, $9,110.14, confirming its validity as a simplified alternative to the manual formula.

Tracking Annual Growth Over Time

While calculating the final value is useful, investors often need to track how the investment grows year-over-year to analyze performance and milestones. This requires setting up a sequential table where the compound interest formula is applied iteratively for each year, allowing the user to observe the accelerating nature of compound growth.

To achieve this, we create a table with a column for the Year (1 through 10) and a corresponding column for the Ending Value. When replicating the formula down a column, it is crucial to use a combination of absolute and relative cell references. The Principal (P) and Annual Interest Rate (r) must remain constant (absolute references, e.g., $B$2 and $B$3), while the number of years (t) must change for each row (relative reference, referencing the year column).

The following screenshot illustrates this detailed year-by-year setup. Column F provides the exact formula used in the corresponding cells in Column E, demonstrating the necessary use of dollar signs ($) for absolute references to fix the principal and rate values across the series of calculations.

Note: Column F shows the formula we used in each corresponding cell in Column E:

From this detailed output, we can observe the annual acceleration of the investment value:

- At the end of year 1, the investment is worth $5,309.16.

- At the end of year 2, the investment is worth $5,637.43.

- At the end of year 3, the investment is worth $5,986.00.

- The incremental growth in value increases with each successive year, a characteristic signature of compound interest applied at a high frequency (daily compounding).

This annual tracking allows for advanced analysis, such as calculating the annual percentage yield (APY) or determining the exact period required to double the initial principal, providing powerful insights into the long-term viability of the investment strategy.

Visualizing Investment Performance

A table of numbers, while accurate, often fails to convey the dramatic effect of compounding over time. By transforming the annual growth data into a chart, we can instantly visualize the non-linear, exponential acceleration of the investment’s value. This visual representation is an indispensable tool for presentations and personal financial planning.

To visualize the investment growth trajectory over the 10-year period, the process is simple within Excel. First, highlight the data range containing the years (optional, but helpful for labels) and the corresponding ending investment values (e.g., the cells in the range E2:E11 from the example above). Next, navigate to the Insert tab located along the top ribbon interface.

Within the Charts group on the Insert ribbon, click the option for the 2-D Column Chart. Excel will automatically generate a bar graph where the x-axis corresponds to the implicit period (Year 1 through 10) and the vertical height of the bars represents the calculated investment value at the end of that specific year.

As clearly demonstrated in the visualization, the bars grow incrementally larger as the investment term progresses. The x-axis shows the year index, and the height of the bars directly correlates to the increasing investment value achieved due to the consistent daily compounding of the annual interest rate. This visual slope powerfully illustrates the fundamental advantage of high-frequency compound interest.

Cite this article

stats writer (2025). How to Easily Calculate Daily Compound Interest in Excel. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-to-calculate-daily-compound-interest-in-excel/

stats writer. "How to Easily Calculate Daily Compound Interest in Excel." PSYCHOLOGICAL SCALES, 30 Nov. 2025, https://scales.arabpsychology.com/stats/how-to-calculate-daily-compound-interest-in-excel/.

stats writer. "How to Easily Calculate Daily Compound Interest in Excel." PSYCHOLOGICAL SCALES, 2025. https://scales.arabpsychology.com/stats/how-to-calculate-daily-compound-interest-in-excel/.

stats writer (2025) 'How to Easily Calculate Daily Compound Interest in Excel', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-to-calculate-daily-compound-interest-in-excel/.

[1] stats writer, "How to Easily Calculate Daily Compound Interest in Excel," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, November, 2025.

stats writer. How to Easily Calculate Daily Compound Interest in Excel. PSYCHOLOGICAL SCALES. 2025;vol(issue):pages.