Table of Contents

Exponential smoothing is a sophisticated statistical methodology employed extensively in quantitative analysis to refine time series data. By mitigating the impact of erratic fluctuations and highlighting persistent underlying patterns, this technique allows analysts to generate reliable short-term predictions. In the context of modern business intelligence, exponential smoothing serves as a critical bridge between raw historical data and actionable future insights. Unlike simple moving averages, which weight all historical data points equally, this method applies exponentially decreasing weights over time, ensuring that the most recent observations have the highest impact on the forecast.

The primary utility of this technique lies in its ability to filter out what mathematicians refer to as random noise. Most real-world datasets, particularly those related to sales, stock prices, or consumer behavior, are characterized by significant volatility—visible as sharp peaks and deep valleys in a line chart. By applying a smoothing constant, we can effectively “iron out” these inconsistencies, revealing the genuine trend estimation that might otherwise be obscured by temporary anomalies. This clarity is essential for organizations that require precision in inventory management, financial budgeting, and strategic resource allocation.

Executing this procedure within Microsoft Excel is remarkably efficient, thanks to the software’s built-in analytical capabilities. While the manual calculation of these values can be labor-intensive, the platform provides automated tools that handle complex algorithms with minimal user input. This guide provides an exhaustive walkthrough for performing this analysis, ensuring that even users without an advanced background in econometrics can produce professional-grade forecasts. By following a structured approach, you can transform a standard spreadsheet into a powerful predictive engine that informs high-level decision-making processes.

The Mathematical Logic of Exponential Smoothing

To fully appreciate how exponential smoothing functions, one must understand the linear combination that forms its foundation. The technique operates on a recursive principle, where each new forecast is a function of the previous actual value and the previous forecast. This creates a feedback loop that continuously adjusts for error, allowing the model to adapt to shifts in the data environment over time. The mathematical expression of this relationship is essential for those who wish to customize their models beyond the default settings provided by standard software packages.

The fundamental formula for determining the forecasted value is expressed as follows:

Ft = αyt-1 + (1 – α) Ft-1

In this equation, the variables represent specific components of the time series model:

- Ft: This represents the forecasted value for the current time period, designated as t.

- α (Alpha): This is the smoothing constant, a coefficient between 0 and 1 that dictates the weight assigned to the most recent data.

- yt-1: This denotes the actual observed data value from the immediately preceding time period.

- Ft-1: This is the forecasted value that was generated for the previous time period, t-1.

The selection of the alpha value is the most critical decision in the smoothing process. A smaller alpha value places more weight on the historical forecast, resulting in a significantly smoother line that is less reactive to recent changes. Conversely, a larger alpha value places more emphasis on the most recent actual data, making the forecast highly responsive to recent fluctuations. Understanding this trade-off between stability and responsiveness is key to selecting a model that accurately reflects the dynamics of your specific industry or dataset.

Structuring Your Data for Analysis in Excel

Before initiating any data analysis, it is imperative to ensure that your information is organized in a logical and accessible format. Microsoft Excel requires data to be arranged in contiguous rows or columns for the smoothing tool to function correctly. Typically, this involves creating a table where the first column represents the time interval—such as days, months, or quarters—and the second column contains the corresponding numerical values you wish to forecast.

Consider a scenario where a business needs to analyze its performance over a period of ten sales cycles. The accuracy of the forecasting model depends entirely on the integrity of this initial input. Ensure there are no missing values or non-numeric characters within the data range, as these can cause errors during the computation process. Once the data is entered, it is often helpful to visualize the raw data using a simple line chart to identify any obvious outliers or seasonal trends that might require special attention before smoothing is applied.

To begin the smoothing process, navigate to the main ribbon in Excel and locate the “Data” tab. This section contains the advanced analytical features necessary for complex computations. If you do not see the “Data Analysis” option on the far right of the ribbon, you may need to enable the Analysis ToolPak. This is a free add-in provided by Microsoft that includes a suite of financial, statistical, and engineering data analysis tools designed to save time and reduce manual entry errors.

Accessing the Exponential Smoothing Tool

With your data properly formatted and the Analysis ToolPak active, you are ready to proceed with the technical execution. The first step involves activating the analysis interface. Click on the Data Analysis button, which will trigger a pop-up window containing a comprehensive list of available statistical procedures. This list includes everything from ANOVA to regression analysis, demonstrating the breadth of Excel’s analytical capabilities.

Scroll through the options in the dialog box until you find the entry for Exponential Smoothing. Selecting this option and clicking “OK” will open a specific configuration menu where you will define the parameters of your model. It is at this stage that you will tell the software which data points to analyze and how aggressively it should smooth the resulting output. Precision during this step is vital, as incorrect range selection is a common source of invalid results in spreadsheet modeling.

The configuration window is designed to be intuitive but requires careful attention to detail. You will be prompted to input the “Input Range,” which is the cell range containing your actual data values. Additionally, if your data range includes a header (e.g., “Sales”), ensure you check the “Labels” box so Excel interprets the first row as text rather than a numerical value. Setting these parameters correctly ensures that the generated data set is accurate and professionally formatted from the outset.

Configuring the Damping Factor and Ranges

The most important parameter in the configuration window is the Damping Factor. In Excel’s implementation of exponential smoothing, the damping factor is defined as 1 minus the smoothing constant (1-α). This is a frequent point of confusion for many users. For example, if your objective is to use a smoothing constant (alpha) of 0.2, you must enter 0.8 as your damping factor. This inverse relationship is fundamental to how the Excel algorithm processes the weighted average of your time series.

To finalize the setup, you must define the following elements in the dialog box:

- Input Range: Select the cells that contain the historical values you wish to smooth.

- Damping Factor: Input the value (1-α). A higher damping factor (closer to 1) results in more significant smoothing, while a lower value (closer to 0) keeps the forecast closer to the actual data.

- Output Range: Designate a specific location in your worksheet where the new values should be placed. Positioning these next to the original data facilitates easy comparison and verification.

- Chart Output: Check this box to automatically generate a data visualization that overlays the forecasted trend onto the original data points.

Once you click “OK,” Excel will perform the calculations and populate the designated output range. You will notice that the very first cell in the forecasted column contains a #N/A error. This is not a malfunction; rather, it is a mathematical necessity. Because the smoothing formula relies on the previous period’s forecast, there is no antecedent data available for the first entry in the series to calculate a result. In subsequent cells, the linear combination of previous values will produce the desired smoothed results.

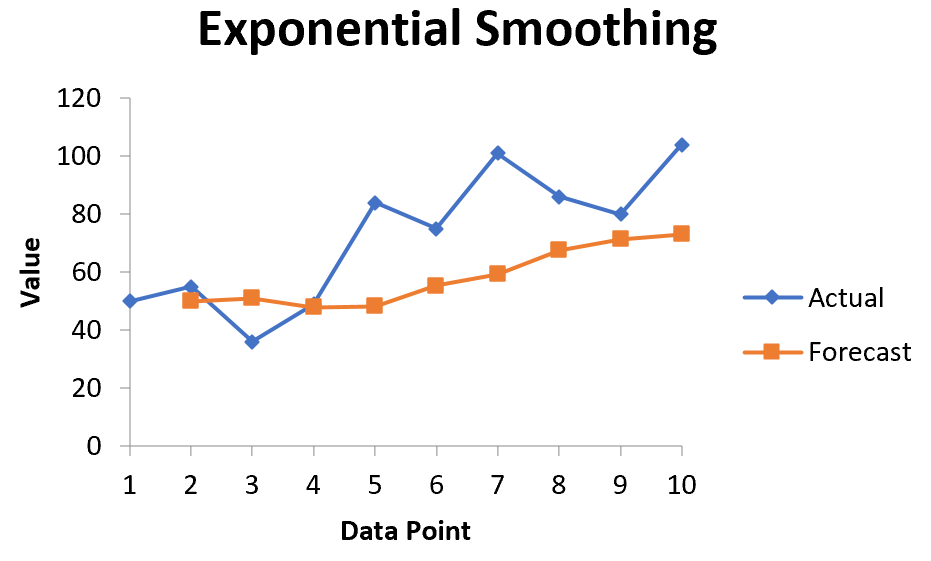

Interpreting the Smoothed Results and Charting

After the computation is complete, Excel provides both a table of values and a visual representation of the data. The resulting chart is an invaluable tool for data analysis, as it allows you to immediately see how well the model fits the historical trend. The “Actual” line will likely show the original volatility, while the “Forecast” line will appear as a more stable, moderated version of that same data. This visual clarity is what makes exponential smoothing such a popular choice for executive reports and presentations.

When reviewing the output, pay close attention to the “lag” that often occurs in smoothed data. Because the forecast is a weighted average of past events, it tends to trail behind significant shifts in the actual data. This is a known characteristic of the simple exponential smoothing method. If your data exhibits a strong upward or downward trend estimation or distinct seasonal patterns, you may eventually need to explore more advanced techniques, such as double or triple exponential smoothing, also known as the Holt-Winters method.

However, for general purposes and noise reduction, the standard output provided by Excel is remarkably effective. It allows analysts to identify the “signal” within the “noise,” providing a clearer picture of whether a business is truly growing or if a recent spike in performance was merely a random occurrence. By having the data side-by-side with the chart, you can perform a quantitative audit of the results to ensure they align with your expectations and the mathematical constraints of the alpha value you selected.

Optimizing the Smoothing Constant for Accuracy

A common challenge for analysts is determining the optimal alpha value for a specific dataset. Experimentation is often the best approach to find the balance between sensitivity and stability. By running the tool multiple times with different damping factors—such as 0.2, 0.5, and 0.8—you can observe how the forecast line changes. A smaller alpha (larger damping factor) will result in a line that is nearly flat, representing the long-term average, while a larger alpha (smaller damping factor) will track the raw data much more closely.

In professional environments, this optimization is often done by calculating the Mean Squared Error (MSE) or the Mean Absolute Error (MAE) for different alpha values. These metrics provide a numerical score for the accuracy of your forecast, allowing you to choose the smoothing constant that minimizes the difference between the actual and predicted values. While Excel’s basic tool doesn’t automate this optimization, you can easily set up a few formulas to calculate these errors yourself, thereby adding a layer of scientific rigor to your forecasting process.

Ultimately, the goal of exponential smoothing in Excel is to facilitate better decision-making. Whether you are predicting next month’s sales, estimating future demand for a product, or trying to understand financial market trends, this tool provides a reliable, repeatable framework for analysis. By mastering the relationship between the smoothing constant and the damping factor, and by leveraging the power of the Analysis ToolPak, you can ensure that your forecasts are grounded in sound statistical principles and presented with professional clarity.

Cite this article

stats writer (2026). How to Forecast Data Trends with Exponential Smoothing in Excel. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-do-i-perform-exponential-smoothing-in-excel/

stats writer. "How to Forecast Data Trends with Exponential Smoothing in Excel." PSYCHOLOGICAL SCALES, 7 Mar. 2026, https://scales.arabpsychology.com/stats/how-do-i-perform-exponential-smoothing-in-excel/.

stats writer. "How to Forecast Data Trends with Exponential Smoothing in Excel." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/how-do-i-perform-exponential-smoothing-in-excel/.

stats writer (2026) 'How to Forecast Data Trends with Exponential Smoothing in Excel', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-do-i-perform-exponential-smoothing-in-excel/.

[1] stats writer, "How to Forecast Data Trends with Exponential Smoothing in Excel," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Forecast Data Trends with Exponential Smoothing in Excel. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.