Table of Contents

Understanding Residuals in Linear Models

The primary goal of linear regression is to find the best linear relationship that describes the association between a dependent variable and one or more independent variables. While the resulting regression line provides the optimal fit according to criteria like Ordinary Least Squares (OLS), it rarely passes exactly through every single observed data point. The concept of the residual is central to understanding the precision and error of this fitted relationship. Mathematically, a residual is defined as the vertical distance between an actual observed value ($Y_i$) and the corresponding predicted value ($hat{Y}_i$) generated by the model. This difference represents the variation in the dependent variable that remains unexplained by the predictor variables included in the model.

A thorough analysis of these residuals is absolutely essential for diagnosing the quality and validity of any statistical model. If the underlying assumptions of the linear model are met—specifically, that the errors are independent, identically distributed, and normally distributed with a mean of zero—the residuals themselves should exhibit a random, unstructured distribution. Conversely, observing specific patterns, trends, or unequal variance (a condition known as heteroscedasticity) within the residuals serves as a clear diagnostic signal that the model is likely misspecified or that certain assumptions have been violated.

The ability to quickly and accurately extract these values is paramount for performing diagnostic checks. The R statistical programming environment simplifies this process significantly through its model fitting functions. By obtaining the vector of residuals, analysts gain the necessary data to perform graphical assessments, statistical tests (such as the Breusch-Pagan test for heteroscedasticity), and other advanced diagnostics, ensuring that the final conclusions drawn from the linear regression are reliable and trustworthy.

The Role of the R lm() Function

In R, the lm() function is the standard tool used to fit and analyze linear models. When a model is fitted using this function (e.g., fit <- lm(Y ~ X, data=df)), the output is not just a summary of coefficients, but a rich, complex object belonging to the S3 class lm. This lm object is structured as a list, containing every piece of information derived from the model estimation process, including coefficient estimates, standard errors, degrees of freedom, the formula used, the fitted values, and the calculated residuals.

Due to its list structure, the model object allows for highly efficient and direct access to any of its components using the dollar sign ($) operator followed by the specific element name. For linear models created by lm(), the vector containing the differences between observed and predicted values is always stored under the element named residuals. Therefore, accessing fit$residuals provides immediate retrieval of this critical diagnostic data. This method is particularly popular among analysts who require quick integration of residuals into subsequent calculations or plots.

While direct access via the $ operator is valid and fast, R also provides generic accessor functions designed for robust interaction with model objects. The resid() or residuals() functions are preferred when aiming for code that is generalized and maintains compatibility across various modeling platforms within R (e.g., handling models from different packages). For an lm() object named fit, both fit$residuals and resid(fit) will return the exact same vector of residuals, confirming that analysts have flexibility in their choice of syntax for extraction.

Methods for Extracting Residuals

Once a linear model has been established, the process of extracting the residuals is fundamentally simple, relying on two primary methods within the R environment. Both methods yield an equivalent vector where each element corresponds directly to the residual of the observation at the same index in the original data set. Selecting which method to use often comes down to personal preference or the need for generic function applicability.

The most direct and widely used technique, particularly for immediate manipulation, is accessing the internal structure of the model object using the dollar sign accessor. This approach leverages the knowledge that the lm() object, stored in a variable like fit, contains a named component explicitly designated for residuals. This method is demonstrated below:

To directly access the residuals vector from the lm() function output in R, assuming the model object is named fit, utilize the following syntax:

fit$residualsThis syntax is highly efficient because it bypasses the need for calling a function, immediately returning the numerical vector containing all residuals calculated during the fitting of the linear regression model.

The alternative method involves employing the generic accessor function, resid(). Unlike direct access, this function is part of R’s standard statistical package and is designed to interface correctly with various types of model outputs, not just lm() objects. By simply passing the model object fit to the function, resid(fit) performs the necessary internal checks and extracts the residuals vector. This function-based approach is often favored in production code or automated scripting due to its reliability and adherence to R‘s object-oriented principles.

Practical Example: Multiple Regression in R

To illustrate the extraction process, we will work through a concrete example using multiple linear regression. This example involves predicting a quantitative outcome using two distinct predictor variables, a common scenario in applied statistics. We hypothesize that a player’s points scored can be modeled by their playing time and the number of fouls committed, necessitating the use of the lm() function with multiple covariates.

The steps that follow mirror a typical data analysis pipeline: first, creating a structured data set; second, defining the mathematical relationship to be tested; and finally, executing the model fitting and subsequent residual extraction. This ensures that every component of the process, from data initialization to the isolation of diagnostic errors, is clearly demonstrated. The resulting residuals will then be used for diagnostic checks to confirm the validity of our predictive model.

This hands-on demonstration emphasizes that regardless of the complexity of the linear model—whether simple or multiple regression—the methodology for extracting the raw error terms remains identical, utilizing the inherent structure of the lm() output object. We will focus specifically on the direct extraction method, fit$residuals, for its brevity and efficiency in interactive sessions.

Setting Up the Data and Model Specification

Our first task is to set up the dataset in R. We create a data frame named df, which simulates performance metrics for 10 basketball players. This data frame includes three variables: minutes (time played), fouls (total fouls committed), and points (total score), where points will serve as our dependent variable.

# Create the data frame containing performance metrics for 10 observations df <- data.frame(minutes=c(5, 10, 13, 14, 20, 22, 26, 34, 38, 40), fouls=c(5, 5, 3, 4, 2, 1, 3, 2, 1, 1), points=c(6, 8, 8, 7, 14, 10, 22, 24, 28, 30)) # Display the created data frame to verify input structure df minutes fouls points 1 5 5 6 2 10 5 8 3 13 3 8 4 14 4 7 5 20 2 14 6 22 1 10 7 26 3 22 8 34 2 24 9 38 1 28 10 40 1 30

We are now ready to define the specific relationship we wish to model. We hypothesize a relationship where points is predicted by a linear combination of minutes and fouls. This relationship is mathematically expressed as a multiple linear regression model:

points = $beta_{0} + beta_{1}(text{minutes}) + beta_{2}(text{fouls}) + epsilon$. The lm() function handles the estimation of the intercept ($beta_{0}$) and the slope coefficients ($beta_{1}$ and $beta_{2}$) based on the observed data, leaving the remaining unexplained variation captured by the residuals ($epsilon$). The R formula syntax simplifies this model specification to points ~ minutes + fouls.

Executing the lm() Fit and Extraction

The model fitting process is executed by passing the formula and the data frame to the lm() function. We assign the resultant model object to the variable fit. This object holds all the statistical output necessary for further diagnostic analysis.

# Fit the multiple linear regression model

fit <- lm(points ~ minutes + fouls, data=df)

The crucial step for obtaining the prediction errors is the extraction of the residuals. Using the direct access method, fit$residuals, we retrieve the vector containing the calculated residual for each of the 10 players included in the model fitting:

# Extract residuals directly from the model object

fit$residuals

1 2 3 4 5 6 7

2.0888729 -0.7982137 0.6371041 -3.5240982 1.9789676 -1.7920822 1.9306786

8 9 10

-1.7048752 0.5692404 0.6144057

The output shows 10 residual values, one for each observation (player) in our initial data frame. These numbers represent the raw error in the model’s prediction of points. A positive value indicates that the player scored more points than the model predicted (under-prediction), while a negative value indicates the player scored fewer points than predicted (over-prediction).

Interpreting the Residual Output

The numerical vector of residuals provides essential insights into how well the model performed at the individual observation level. Since there were 10 observations used to fit the model, we necessarily obtain 10 corresponding residuals. The magnitude of the residual indicates the size of the prediction error, and the sign indicates the direction of that error relative to the actual observation.

For detailed interpretation, consider the first few data points: The first observation has a residual of approximately 2.089. This positive value means that for Player 1, the actual score was 2.089 units higher than the score calculated by the regression line. This player performed slightly better than the model expected given their minutes and fouls. Conversely, the second observation has a residual of -0.798. This negative value indicates the model slightly over-predicted the points scored by Player 2. The fourth observation exhibits the largest magnitude error, -3.524, signaling the greatest discrepancy between actual and predicted points in our sample, and representing a significant over-prediction.

We can summarize the direction and magnitude of the error for several players:

- The first observation (Index 1) has a positive residual (2.089), indicating the model under-predicted the outcome.

- The sixth observation (Index 6) has a negative residual (-1.792), meaning the model over-predicted the actual points scored.

- The seventh observation (Index 7) has a positive residual (1.931), similar to the first observation, suggesting another instance of under-prediction.

While interpreting individual residuals is informative, the collective analysis of the residual set—particularly through graphical methods—is crucial for assessing the adherence to fundamental statistical assumptions and ensuring the overall model fit is sound.

Visual Analysis: Creating a Residual vs. Fitted Plot

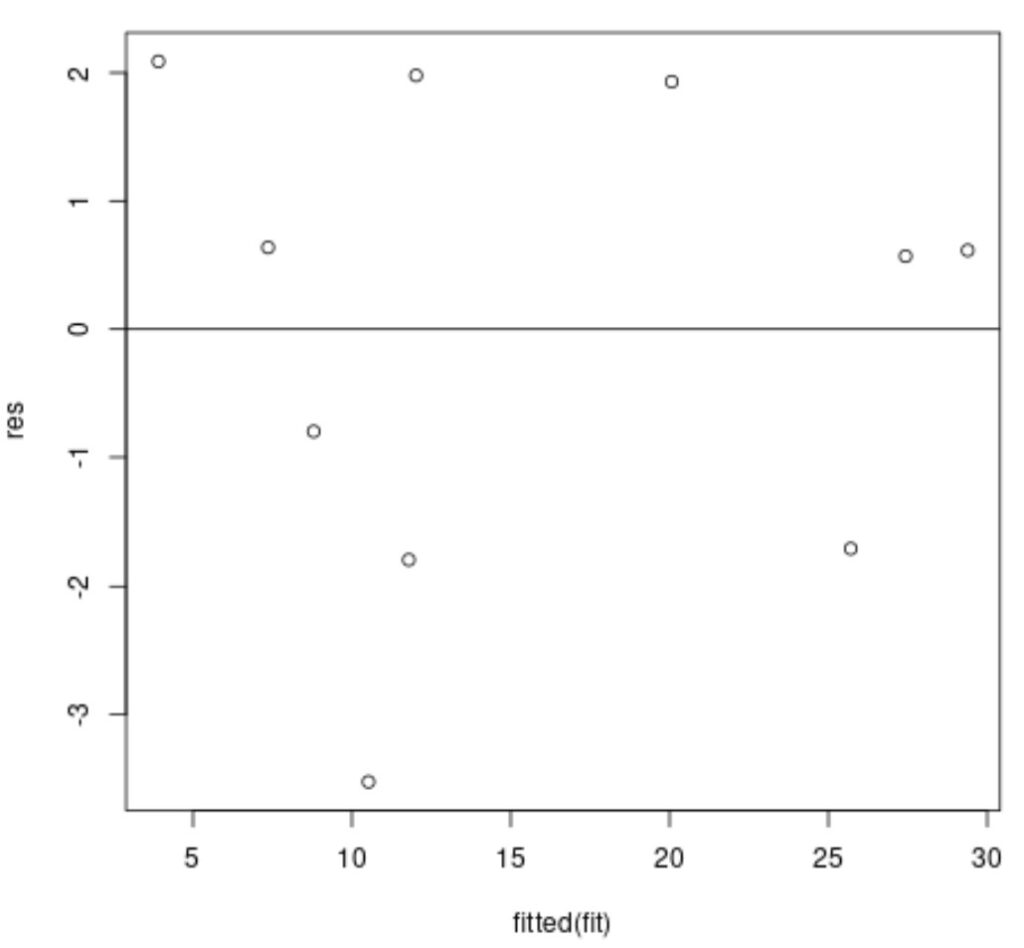

To move beyond numerical review and conduct robust diagnostic checks, the Residual vs. Fitted Values plot is indispensable. This visualization plots the residuals (Y-axis) against the model’s predicted or fitted values ($hat{Y}_i$ on the X-axis). Its primary function is to provide a graphical test of linearity and the assumption of homoscedasticity (constant variance).

To generate this plot in R, we utilize the plot() function, passing the fitted values and the extracted residuals as arguments. We also include the abline() function to draw a reference line at $Y=0$. This horizontal line represents the ideal scenario where all prediction errors are zero, providing a clear visual center for evaluating the scatter of the residuals.

# Store residuals in a temporary variable for clarity res <- fit$residuals # Produce the residual vs. fitted plot plot(fitted(fit), res, main="Residuals vs. Fitted Values Plot", xlab="Fitted Values (Predicted Points)", ylab="Residuals (Prediction Error)") # Add a horizontal reference line at 0 for visual reference abline(0,0, col="red")

The resultant visualization enables the analyst to quickly identify patterns that suggest problems with the model specification.

A successful linear regression model should display a pattern where the residuals are randomly scattered both above and below the zero line, forming a roughly horizontal band of points across the entire range of fitted values. Any systematic deviation from this horizontal, random band warrants closer investigation and potential remedial action.

Evaluating Model Assumptions Using Residuals

The residual plot is the cornerstone of regression diagnostics, specifically designed to verify two core assumptions of the OLS framework: the assumption of linearity and the assumption of constant variance (homoscedasticity). Failing these checks indicates that the model results may be inefficient or biased.

To confirm the assumption of linearity, the residuals must show no discernible trend when plotted against the fitted values. If a curvilinear pattern emerges—such as a parabolic or S-shape—it suggests that a linear model is inappropriate for the data, and transformation of variables or the inclusion of polynomial terms may be required. In our example plot, the points appear to be scattered without a clear curvature, suggesting the linear relationship assumption holds.

The check for homoscedasticity requires that the variance of the residuals remains consistent across all levels of the fitted values. If the spread (or vertical distance) of the residuals increases as the fitted values increase (a fan-out shape), or decreases (a cone shape), the data exhibits heteroscedasticity. This condition violates the OLS assumption that the errors have constant variance, leading to inefficient standard errors and potentially incorrect hypothesis testing. Ideally, the residuals should form a uniform, horizontal band. In the provided plot, the residuals seem to be randomly scattered about zero with relatively constant vertical spread, suggesting the assumption of constant error variance is likely met. This confirms that our linear model, fitted using the lm() function, is performing adequately based on these key diagnostic criteria.