Table of Contents

Understanding the Foundations of Covariance and Statistical Analysis

In the vast landscape of statistics and data analysis, the ability to quantify the relationship between multiple variables is paramount. A covariance matrix serves as a robust mathematical framework designed to analyze these dependencies within a dataset. By examining how variables change in relation to one another, researchers can discern whether an increase in one variable corresponds to a predictable increase or decrease in another. This fundamental concept is essential for any professional working in data science or machine learning, as it forms the basis for more complex techniques such as Principal Component Analysis and portfolio optimization.

The primary utility of a covariance matrix lies in its ability to summarize the variance and covariance of a multidimensional dataset into a single, organized structure. In Python, this process is streamlined through the use of the NumPy library, a cornerstone of scientific computing. The library provides a built-in function specifically designed for this purpose, allowing users to pass raw data and receive a structured matrix of values. This efficiency enables rapid exploration of data features and provides immediate insights into the underlying linear associations between different columns or observations.

To grasp the utility of this tool, one must understand that covariance measures the directional relationship between the linear movements of two random variables. Unlike correlation, which is standardized, covariance is expressed in the original units of the variables, making it a raw but powerful indicator of joint variability. When dealing with large datasets containing dozens of variables, manual calculation becomes impossible, which is why Python and its specialized libraries are indispensable for modern analytical workflows. By utilizing these tools, we can transform abstract numbers into meaningful indicators of systemic behavior.

The Role of Covariance Matrices in Data Science

A covariance matrix is essentially a square matrix that provides a comprehensive overview of the pairwise covariances between several variables. This structure is particularly useful because it organizes information logically: the diagonal elements represent the variance of each individual variable, while the off-diagonal elements represent the covariance between variable pairs. This dual-purpose representation allows analysts to observe both the spread of individual data points and the strength of their linear connections simultaneously, making it a prerequisite for many advanced statistics models.

In practical applications, understanding how different variables are related helps in identifying patterns that might otherwise remain hidden. For instance, in an educational context, a covariance matrix can reveal if high performance in mathematics is typically accompanied by similar performance in sciences. Because the matrix is symmetric, the covariance between variable A and variable B is identical to the covariance between variable B and variable A. This symmetry simplifies the interpretation and ensures that the statistical representation remains consistent across the entire dataset.

The following detailed walkthrough demonstrates how to implement and interpret these concepts within the Python programming environment. By following a structured approach, we can move from raw data collection to a finalized heatmap visualization, ensuring that each step of the mathematical transformation is understood and verified. This process is not merely about writing code; it is about developing a rigorous analytical mindset that treats data as a interconnected system rather than isolated values.

Prerequisites and Initial Environment Setup

Before diving into the calculation of a covariance matrix, it is necessary to establish a functional programming environment. Python is the preferred language for this task due to its extensive ecosystem of data-centric libraries. The most critical library for this specific exercise is NumPy, which provides the high-performance array objects and mathematical functions needed to handle linear algebra operations efficiently. Ensuring that your local environment or Jupyter Notebook has these tools installed is the first step toward successful data processing.

In addition to NumPy, we will eventually utilize Seaborn and Matplotlib for visualization purposes. While the mathematical output of a covariance matrix is purely numerical, humans are often better at identifying trends through visual representations. Seaborn acts as a high-level interface for Matplotlib, making it significantly easier to create attractive and informative heatmap displays that highlight the magnitude of covariance values through color gradients.

Once the libraries are imported, the logic follows a standard linear algebra workflow. We treat our variables as vectors and our dataset as a collection of these vectors. By structuring the data correctly from the start, we avoid common pitfalls related to dimensionality and axis alignment during the calculation phase. This preparation phase is crucial, as it sets the stage for accurate data analysis and ensures that the subsequent functions receive the data in the expected format.

Step 1: Constructing the Multi-Variable Dataset

The first practical step in our workflow involves the creation of a representative dataset. For this example, we will simulate the academic performance of ten different students across three distinct subjects: math, science, and history. This variety allows us to explore how different academic disciplines might correlate with one another. By defining these scores as lists in Python, we create the raw material necessary for our statistical exploration.

After defining the individual subjects, we consolidate them into a NumPy array. This conversion is vital because NumPy functions are optimized to work with these array structures rather than standard Python lists. The resulting matrix will have rows representing the subjects and columns representing the individual student observations. This layout is standard in many statistical functions, though it is always important to verify the orientation of your data before proceeding with calculations.

import numpy as np math = [84, 82, 81, 89, 73, 94, 92, 70, 88, 95] science = [85, 82, 72, 77, 75, 89, 95, 84, 77, 94] history = [97, 94, 93, 95, 88, 82, 78, 84, 69, 78] data = np.array([math, science, history])

By organizing the data this way, we can easily see the performance spread. For instance, in the math scores, we see a range from 70 to 95, suggesting significant variance. Similarly, the science and history scores show their own unique distributions. The goal of the covariance matrix will be to determine if these distributions move in a synchronized fashion or if they are entirely independent of one another.

Step 2: Executing the Covariance Matrix Calculation

With our dataset prepared, we can now apply the cov() function from the NumPy library. This function is highly versatile and handles the heavy lifting of the covariance formula. A critical parameter to consider here is the strong>bias argument. Setting bias = True allows us to calculate the population covariance rather than the sample covariance. This distinction is important in statistics, as it determines whether the divisor in the formula is N or N-1.

The output of this function is a 3×3 matrix because we have three variables (math, science, and history). Each cell in the matrix corresponds to the relationship between a specific pair of subjects. The diagonal elements are especially noteworthy as they represent the variance of a subject with itself. This mathematical property is a hallmark of the covariance matrix and serves as a internal check for data consistency.

np.cov(data, bias=True)

array([[ 64.96, 33.2 , -24.44],

[ 33.2 , 56.4 , -24.1 ],

[-24.44, -24.1 , 75.56]])

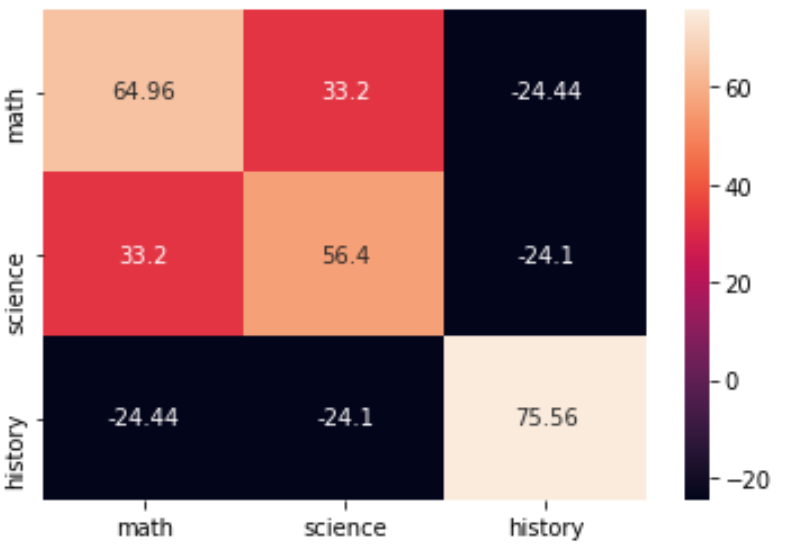

The resulting values give us immediate quantitative data. For example, the value at the intersection of the first row and first column (64.96) is the variance of the math scores. The value at the intersection of the first row and second column (33.2) is the covariance between math and science. These numbers are the foundation upon which we will build our interpretation of student performance trends.

Step 3: Interpreting the Diagonal and Off-Diagonal Values

Interpreting a covariance matrix requires an understanding of what the specific numbers represent in a real-world context. As previously mentioned, the diagonal values are the variance of each subject. Variance measures how far each number in the set is from the mean. A higher variance indicates that the scores are more spread out, while a lower variance suggests that the students’ scores were more clustered around the average.

- The variance for math scores is 64.96, indicating a moderate spread in student ability.

- The variance for science scores is 56.4, showing the least amount of spread among the three subjects.

- The variance for history scores is 75.56, suggesting the widest range of performance among the students.

The off-diagonal values represent the covariance between different subject pairs. The sign of these numbers (positive or negative) is the most critical piece of information. A positive number indicates a direct relationship: as one score goes up, the other tends to go up as well. Conversely, a negative number indicates an inverse relationship: as one score goes up, the other tends to go down.

- The covariance between math and science is 33.2, a positive value that suggests students who excel in math often excel in science.

- The covariance between math and history is -24.44, indicating a negative trend where high math scores might align with lower history scores in this specific group.

- The covariance between science and history is -24.1, further reinforcing the inverse relationship between the scientific and humanities-based subjects in this dataset.

Step 4: Advanced Visualization with Seaborn Heatmaps

While the numerical matrix is scientifically accurate, it can be difficult to interpret at a glance, especially as the number of variables grows. This is where data visualization becomes essential. By using the heatmap() function from the Seaborn library, we can map the covariance values to colors, making the relationships immediately obvious to the human eye.

In the following code snippet, we use Matplotlib to manage the figure and Seaborn to generate the heatmap. We add annotations to display the actual numbers inside the cells and set the labels to represent our subjects clearly. This turns a dry matrix of numbers into a professional-grade graphic suitable for reports or presentations.

import seaborn as sns import matplotlib.pyplot as plt cov = np.cov(data, bias=True) labs = ['math', 'science', 'history'] sns.heatmap(cov, annot=True, fmt='g', xticklabels=labs, yticklabels=labs) plt.show()

To enhance the visual clarity further, Seaborn allows for customization of the color palette via the cmap argument. Different colormaps can highlight different aspects of the data; for example, a diverging colormap can make it very easy to distinguish between positive and negative covariance values. This flexibility is one of the reasons Python is so popular for data analysis.

sns.heatmap(cov, annot=True, fmt='g', xticklabels=labs, yticklabels=labs, cmap='YlGnBu') plt.show()

Practical Applications and Final Considerations

Generating a covariance matrix is more than just a classroom exercise in statistics; it is a vital step in many real-world data science pipelines. For instance, in finance, covariance is used to calculate the risk associated with a portfolio of stocks. If assets have high positive covariance, they tend to move together, increasing the overall risk. Diversification aims to find assets with low or negative covariance to balance the portfolio.

In the field of machine learning, the covariance matrix is a key component of Principal Component Analysis (PCA). PCA uses the eigenvectors and eigenvalues of the covariance matrix to reduce the dimensionality of data while preserving as much variance as possible. This allows for more efficient model training and helps in visualizing high-dimensional datasets in two or three dimensions.

Ultimately, the combination of NumPy for calculation and Seaborn for visualization provides a powerful toolkit for any analyst. By understanding how to create and interpret these matrices, you gain the ability to look beneath the surface of your data and understand the complex web of interactions that drive your observations. Whether you are analyzing student test scores or complex financial markets, the covariance matrix remains an essential tool in your analytical arsenal.

Cite this article

stats writer (2026). How to Create a Covariance Matrix in Python with NumPy. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-can-i-create-a-covariance-matrix-in-python/

stats writer. "How to Create a Covariance Matrix in Python with NumPy." PSYCHOLOGICAL SCALES, 16 Mar. 2026, https://scales.arabpsychology.com/stats/how-can-i-create-a-covariance-matrix-in-python/.

stats writer. "How to Create a Covariance Matrix in Python with NumPy." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/how-can-i-create-a-covariance-matrix-in-python/.

stats writer (2026) 'How to Create a Covariance Matrix in Python with NumPy', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-can-i-create-a-covariance-matrix-in-python/.

[1] stats writer, "How to Create a Covariance Matrix in Python with NumPy," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Create a Covariance Matrix in Python with NumPy. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.