Table of Contents

How to Effectively Test for Multicollinearity in Stata

Multicollinearity represents a significant challenge in the field of regression analysis, appearing when two or more independent variables in a statistical model exhibit a high degree of linear correlation. In an ideal Ordinary Least Squares (OLS) framework, each predictor should provide unique, non-redundant information to help explain the variation in the dependent variable. When variables are nearly perfect linear combinations of one another, the model struggles to isolate the individual contribution of each regressor, leading to unstable and often misleading results.

The presence of this phenomenon does not necessarily reduce the overall predictive power or R-squared of the model, but it dramatically affects the calculations regarding individual predictors. Specifically, it inflates the standard errors of the coefficient estimates. When standard errors are artificially high, the calculated t-statistics become small, making it difficult to achieve statistical significance even if a relationship truly exists in the population. This lack of precision can lead to a Type II error, where researchers fail to reject a null hypothesis that is actually false.

In the Stata software environment, identifying and correcting for these issues is a streamlined process involving several post-estimation commands. By utilizing metrics such as the Variance Inflation Factor (VIF), researchers can quantify the extent to which the variance of an estimated regression coefficient is increased because of collinearity. This guide provides a comprehensive walkthrough of detecting and mitigating these issues to ensure your linear regression models are robust, reliable, and interpretable.

Understanding the Theoretical Impact of Collinearity

To appreciate why we must test for multicollinearity, one must understand the underlying mechanics of linear regression. When we estimate a model, we are essentially trying to determine how much the response variable changes for every unit change in a specific predictor, holding all other variables constant. If two variables, such as “height” and “shoe size,” move in near-perfect lockstep, the mathematical algorithm cannot “hold one constant” while varying the other. This creates a situation where the model becomes hypersensitive to small changes in the data, resulting in coefficients that may swing wildly from one sample to the next.

The Variance Inflation Factor serves as the primary diagnostic tool in this context. Mathematically, the VIF for a specific variable is calculated by regressing that variable against all other independent variables in the model and then taking the inverse of the tolerance (1 – R-squared). This produces a score that tells us exactly how much the variance of a coefficient is being “inflated.” For instance, a VIF of 10 suggests that the variance of the coefficient is ten times larger than it would be if there were zero correlation between that predictor and the others.

Beyond the inflation of standard errors, high collinearity can lead to “wrong-signed” coefficients. This occurs when a variable that theoretically should have a positive relationship with the outcome suddenly displays a negative coefficient in the regression output. This is often a red flag that the model is suffering from structural redundancy, making the interpretation of individual marginal effects virtually impossible for policy-making or scientific inference.

Practical Implementation: Setting up the Stata Environment

To demonstrate these concepts, we will utilize a classic Stata internal dataset. The “auto” dataset contains various metrics regarding 74 automobiles from 1978, including price, weight, length, and fuel efficiency. These variables are excellent candidates for testing because physical attributes like weight and length are naturally correlated, providing a realistic scenario for a multicollinearity diagnostic check. We begin by clearing the memory and loading the data with a simple system command.

sysuse auto

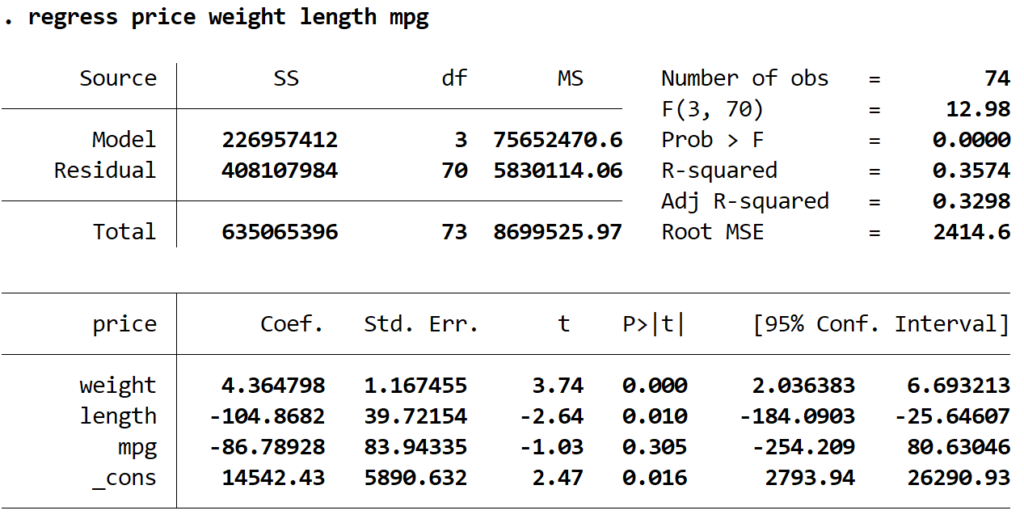

Once the dataset is loaded, we proceed to fit a multiple linear regression model. In this example, we designate “price” as our response variable, while “weight,” “length,” and “mpg” (miles per gallon) serve as our explanatory variables. The objective is to see how these factors influence the market value of the cars. Execute the following command to generate the initial regression output:

regress price weight length mpg

The resulting output provides various statistics, including the coefficients and their associated p-values. At first glance, the model might appear functional, but the standard errors for “weight” and “length” may be larger than expected. To confirm whether these variables are interfering with each other’s performance, we must move beyond the basic regression table and employ specific post-estimation diagnostics designed for Ordinary Least Squares validation.

Executing and Interpreting the VIF Command

After running a regression, Stata stores the results in its memory, allowing us to run the “vif” command immediately. This command does not require any additional arguments; it automatically analyzes the most recently fitted model. The VIF command is the industry standard for detecting multicollinearity because it provides a clear, numerical threshold for decision-making. Run the command as follows:

vif

The output generates a table listing each variable alongside its VIF and the inverse of the VIF, known as the tolerance. Interpreting these results requires adhering to established statistical rules of thumb. Generally, a VIF of 1 indicates a total absence of correlation. Values between 1 and 5 suggest moderate correlation, which is typically acceptable in most social science and economic research. However, when values exceed 5 or 10, it indicates that the standard errors are significantly compromised.

In our specific output, we observe that “weight” and “length” both possess VIF values significantly higher than 5. This suggests that these two variables are essentially conveying the same information regarding the car’s size. Because they are so highly correlated, the model cannot distinguish the effect of an extra inch of length from the effect of an extra pound of weight. This confirms that multicollinearity is indeed a problem in this model, necessitating a strategy for remediation to improve the reliability of our statistical significance tests.

Analyzing Relationships via the Correlation Matrix

When the VIF test identifies a problem, the next logical step is to pinpoint which specific variables are the source of the conflict. While VIF tells us that a variable is correlated with the *rest* of the model, a correlation matrix allows us to see the pairwise relationships between every variable. This is a crucial diagnostic step because it helps researchers decide which variable is redundant and can be safely removed or transformed without losing vital information.

In Stata, the “corr” command generates a matrix showing the Pearson correlation coefficient for every pair of variables. These coefficients range from -1 to +1, where values close to 1 indicate a strong positive linear relationship. By examining the correlations between our predictors and our response variable, we can make an informed choice about which predictor is providing the least “unique” value to the regression. Execute the command below:

corr price weight length mpg

The matrix reveals that “length” and “weight” have a correlation coefficient nearing 0.95, which is exceptionally high. Furthermore, “length” has a weaker correlation with the response variable “price” compared to “weight.” This data-driven insight suggests that “length” is the primary candidate for exclusion. By removing the variable that is highly redundant with others but less correlated with the target, we can effectively mitigate multicollinearity while preserving the model’s overall explanatory power and R-squared.

Strategies for Remediating Collinearity Issues

Once multicollinearity is diagnosed, researchers have several paths forward. The most straightforward approach, as demonstrated in this guide, is variable deletion. By removing one of the highly correlated variables, you simplify the model and restore the stability of the remaining coefficients. This is often the preferred method when two variables are conceptually similar, such as “annual income” and “taxable earnings,” where keeping both adds no real value to the regression analysis.

However, if both variables are theoretically essential to the research question, other techniques may be required. One common method is to combine the correlated variables into a single index or use Principal Component Analysis (PCA) to create a composite score. Another alternative is mean-centering the variables, which involves subtracting the average value from each observation. Centering is particularly effective for reducing collinearity in models that include interaction terms or polynomial powers (e.g., x and x-squared).

Finally, researchers might consider more advanced estimation techniques like Ridge Regression. Ridge regression introduces a small amount of bias into the estimates to significantly reduce the variance, effectively “shrinking” the coefficients to make them more stable. While this moves away from pure OLS, it is a powerful tool when multicollinearity is unavoidable due to the nature of the data. For most standard applications in Stata, however, refining the variable selection remains the most transparent and interpretable solution.

Refining the Model and Verifying Results

To implement our chosen solution, we re-run the linear regression in Stata, this time omitting the “length” variable. The goal is to observe how the exclusion of a redundant predictor affects the standard errors and the stability of the remaining variables. We anticipate that the coefficients for “weight” and “mpg” will become more precise, even if the overall R-squared drops slightly. Execute the refined regression command:

regress price weight mpg

Upon reviewing the new output, we check the adjusted R-squared. In our example, it moved from approximately 0.329 to 0.273. While this is a decrease, the trade-off is often worth it for the gain in coefficient reliability. The final step in our workflow is to run the VIF diagnostic one last time to confirm that the multicollinearity has been resolved. This “post-remedy” check is a hallmark of rigorous regression analysis.

vif

The updated VIF table should now show all values well below the critical threshold of 5. With the VIFs now in a healthy range, we can conclude that the model is no longer suffering from the distorting effects of high internal correlation. The p-values and confidence intervals can now be interpreted with much higher confidence, ensuring that the final conclusions of the study are based on sound statistical foundations rather than mathematical artifacts.

Summary of Best Practices for Stata Users

Testing for multicollinearity should be a standard part of every researcher’s diagnostic workflow when performing Ordinary Least Squares regression. By following a structured approach—running the regression, checking VIF, analyzing correlation matrices, and refining the variable list—you ensure that your model remains parsimonious and accurate. Stata provides all the necessary tools to perform these checks with just a few keystrokes, making it accessible for both novice and expert analysts.

Always remember that while a high VIF is a warning sign, it is not a “failed” test. It is a diagnostic signal that prompts further investigation into the data structure. Sometimes, high VIFs are acceptable, especially in models with many control variables where the main predictor of interest is not affected. However, in most explanatory models, maintaining low VIF values is essential for producing statistically significant and reproducible research results.

By mastering commands like “vif,” “corr,” and “regress,” you empower yourself to build more sophisticated and defensible models. Whether you are analyzing economic trends, social behaviors, or engineering data, the ability to detect and solve multicollinearity will significantly elevate the quality of your quantitative output. Continue to explore Stata documentation for user-contributed commands like “collin” to further expand your diagnostic toolkit.

Cite this article

stats writer (2026). How to Test for Multicollinearity in Stata: A Step-by-Step Guide. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-can-i-test-for-multicollinearity-in-stata/

stats writer. "How to Test for Multicollinearity in Stata: A Step-by-Step Guide." PSYCHOLOGICAL SCALES, 9 Mar. 2026, https://scales.arabpsychology.com/stats/how-can-i-test-for-multicollinearity-in-stata/.

stats writer. "How to Test for Multicollinearity in Stata: A Step-by-Step Guide." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/how-can-i-test-for-multicollinearity-in-stata/.

stats writer (2026) 'How to Test for Multicollinearity in Stata: A Step-by-Step Guide', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-can-i-test-for-multicollinearity-in-stata/.

[1] stats writer, "How to Test for Multicollinearity in Stata: A Step-by-Step Guide," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Test for Multicollinearity in Stata: A Step-by-Step Guide. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.