Table of Contents

Introduction to the Durbin-Watson Table and Its Significance in Statistics

In the realm of advanced quantitative research, the Durbin-Watson Table serves as an indispensable reference tool for scholars and data scientists alike. Primarily utilized within the framework of regression analysis, this table provides the foundational benchmarks required to assess the integrity of a statistical model. When researchers construct models to predict outcomes or identify relationships between variables, they must ensure that the underlying assumptions of their chosen method are fully met. One of the most critical assumptions in Ordinary Least Squares (OLS) regression is the independence of residuals. The Durbin-Watson Table provides the specific critical values necessary to test this assumption rigorously.

The core purpose of the Durbin-Watson Table is to assist in the detection of autocorrelation, specifically first-order serial correlation, within the error terms of a model. If error terms are correlated over time or across observations, the model’s output can become misleading, potentially leading to incorrect conclusions regarding the significance of the independent variables. By referencing the table, analysts can compare their calculated test statistic against predetermined thresholds to determine if the relationship between residuals is statistically significant. This process is a hallmark of robust hypothesis testing, ensuring that the results of a study are not merely artifacts of the data’s structure.

Beyond its technical utility, the Durbin-Watson Table represents a bridge between theoretical econometrics and practical application. Whether in finance, biology, or social sciences, the ability to validate a model’s residuals is paramount. The table is structured to accommodate various sample sizes and numbers of regressors, making it a versatile asset in the statistician’s toolkit. By adhering to the standards set by these critical values, researchers can maintain the high level of validity required for peer-reviewed publication and professional decision-making.

Understanding the Concept of Autocorrelation in Regression Models

To fully appreciate the necessity of the Durbin-Watson Table, one must first understand the phenomenon known as autocorrelation. In a standard regression model, we assume that the error associated with one observation is entirely independent of the error associated with any other observation. However, in many real-world datasets—particularly time series data—this assumption is often violated. For example, if we are measuring economic growth over several quarters, an unexpected shock in one quarter is likely to linger into the next, causing the residuals to follow a discernible pattern rather than being randomly distributed.

When positive autocorrelation occurs, the standard error of the regression coefficients tends to be underestimated. This leads to artificially high T-statistics and narrow confidence intervals, which can deceive a researcher into believing a variable is statistically significant when it is not. This is often referred to as a Type I error in hypothesis testing. Conversely, negative autocorrelation, though less common in social sciences, occurs when a positive error in one period is consistently followed by a negative error in the next, which can also distort the reliability of the model’s inferences.

The Durbin-Watson test specifically targets first-order autocorrelation, meaning it looks for a relationship between a residual and the residual immediately preceding it. By identifying these patterns early in the diagnostic phase of regression analysis, an analyst can take corrective measures. These measures might include adding more independent variables, transforming the existing data, or employing different estimation techniques like feasible generalized least squares. The Durbin-Watson Table is the primary instrument used to diagnose these issues before they compromise the entire study.

The Mathematical Mechanics of the Durbin-Watson Statistic

The Durbin-Watson statistic, often denoted as d, is calculated through a specific formula that compares the squared differences of successive residuals to the sum of the squared residuals. Mathematically, the value of d will always fall between 0 and 4. A value of 2 indicates that there is no autocorrelation detected in the sample. As the value of d moves toward 0, it suggests the presence of positive serial correlation. Conversely, as the value approaches 4, it indicates the presence of negative serial correlation. This numerical range provides a quick diagnostic snapshot for the researcher.

While the calculation of the d statistic is straightforward and often performed automatically by statistical software, the interpretation of this number is where the Durbin-Watson Table becomes essential. The distribution of the d statistic depends on the matrix of independent variables, which means there is no single critical value that applies to all models. Instead, the table provides two distinct bounds: a lower bound (dL) and an upper bound (dU). These bounds are determined by the number of observations (n) and the number of explanatory variables (k) in the regression analysis.

Understanding these bounds is crucial for accurate statistical significance testing. If the calculated d is less than dL, the null hypothesis of no autocorrelation is rejected in favor of the presence of positive correlation. If d is greater than dU, the researcher fails to reject the null hypothesis. However, if the value falls between dL and dU, the test is considered inconclusive. This “zone of indecision” is a unique characteristic of the Durbin-Watson test, highlighting the importance of having a high-quality Durbin-Watson Table to pinpoint these specific thresholds for various alpha levels.

Navigating and Using the Durbin-Watson Critical Values Table

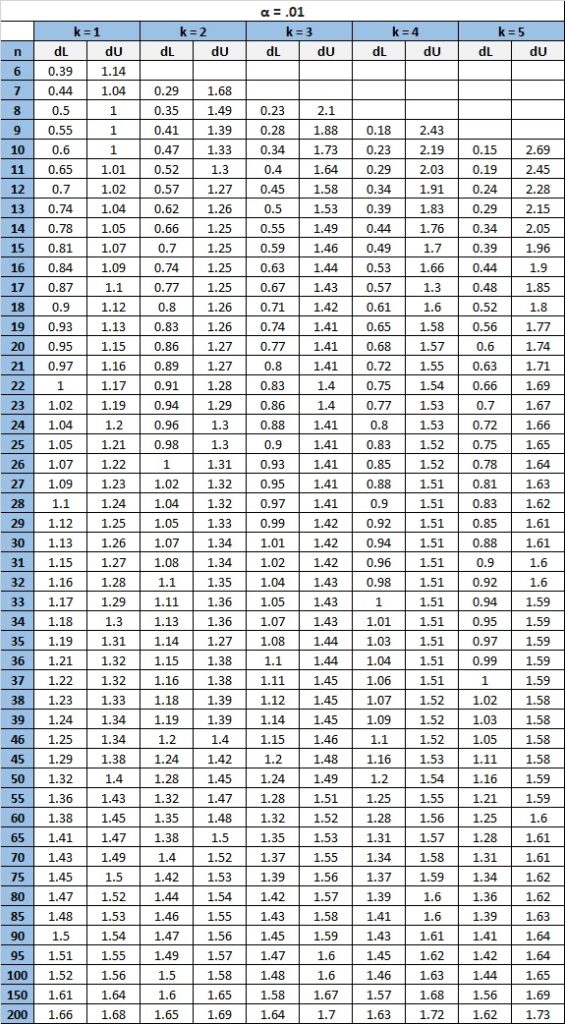

To use a Durbin-Watson Table effectively, a researcher must first identify three key parameters: the sample size (n), the number of independent variables (k) excluding the intercept, and the desired alpha level (usually 0.05 or 0.01). The table is typically organized with rows representing the sample size and columns representing the number of regressors. At the intersection of these two points, the table provides two values: dL and dU. These are the critical boundaries that define the rejection and non-rejection regions for the test.

The process begins by locating the correct table for the chosen alpha level. For instance, if a researcher is conducting a study with 50 observations and 3 independent variables at a 5% significance level, they would look for the row labeled “50” and the column labeled “3.” The resulting dL and dU values will then be compared against the d statistic generated from the regression analysis. This systematic approach ensures that the diagnostic process is standardized and reproducible, which is fundamental to the scientific method.

In addition to checking for positive autocorrelation, the Durbin-Watson Table can also be used to test for negative autocorrelation. This is done by calculating the value of (4 – d) and comparing it against the same dL and dU critical values. If (4 – d) is less than dL, negative autocorrelation is present. This dual functionality makes the table a comprehensive resource for evaluating error structures in linear models. Below are the critical value tables commonly used in statistical practice:

The Role of Sample Size and Independent Variables in Critical Value Determination

The sensitivity of the Durbin-Watson statistic to the structure of the data is one of its most defining features. As the sample size (n) increases, the critical values dL and dU tend to converge toward the value of 2, making it easier to distinguish between random noise and actual autocorrelation. In very small samples, the gap between dL and dU is often wide, which frequently leads to inconclusive results. This reflects the inherent difficulty in identifying patterns within limited data points, a common challenge in longitudinal studies with infrequent data collection.

The number of independent variables (k) also plays a significant role in determining the critical values. Generally, as more regressors are added to the model, the dU value increases. This shift accounts for the increased complexity of the model and the potential for the residuals to be influenced by a wider array of factors. It is vital for researchers to count their variables accurately—specifically focusing on the number of slope coefficients—to ensure they are referencing the correct column in the Durbin-Watson Table.

Furthermore, the choice of the alpha level determines the strictness of the test. A 1% alpha level (0.01) is much more conservative than a 5% level (0.05), requiring stronger evidence to reject the null hypothesis of no autocorrelation. The Durbin-Watson Table is typically provided for both levels to allow researchers to choose the threshold that best fits their field’s standards or the specific risks associated with making a false-positive discovery. Mastering the interplay between n, k, and alpha is key to high-level data analysis.

Practical Implications of Autocorrelation on Statistical Inference

When a researcher identifies autocorrelation using the Durbin-Watson Table, the implications for the study’s findings are profound. The primary concern is that the Ordinary Least Squares (OLS) estimators, while still unbiased, are no longer “Efficient.” This means they no longer have the minimum variance among all linear unbiased estimators. Consequently, the standard error values reported by statistical software will be incorrect, which directly impacts the P-value calculations for each variable.

In many cases, positive autocorrelation leads to an overestimation of the R-squared value, giving a false sense of how well the model explains the variance in the dependent variable. This can lead to overconfidence in the predictive power of the regression analysis. For instance, in financial forecasting, failing to account for serial correlation might lead an analyst to believe a specific market indicator is a highly reliable predictor of price movements, when in reality, the perceived relationship is merely a result of the time-ordered nature of the data.

To mitigate these risks, researchers must use the Durbin-Watson Table as a gateway to further diagnostic testing and model refinement. If the test indicates significant autocorrelation, the researcher might need to implement Cochrane-Orcutt estimation or use Newey-West standard errors to produce more reliable results. These advanced techniques adjust for the correlation in the error terms, restoring the validity of the statistical inferences and ensuring that the final conclusions of the research are grounded in sound mathematical practice.

Steps for Conducting the Durbin-Watson Test in Empirical Research

Executing a proper Durbin-Watson test involves a series of logical steps that integrate software output with the manual use of the Durbin-Watson Table. The process is as follows:

- Step 1: Run the Regression. Perform your linear regression using OLS and ensure that the observations are ordered correctly, especially if the data is a time series.

- Step 2: Calculate the d Statistic. Most statistical software packages (like SPSS, Stata, or R) will provide the Durbin-Watson d statistic as part of the standard regression output.

- Step 3: Define Parameters. Identify your sample size (n) and the number of independent variables (k). Choose your significance level (alpha).

- Step 4: Consult the Table. Locate the dL and dU values in the Durbin-Watson Table corresponding to your parameters.

- Step 5: Compare and Conclude. Compare your calculated d with the table values to determine if you reject or fail to reject the null hypothesis of no autocorrelation.

It is important to note that the Durbin-Watson statistic is only valid for models that include an intercept term. Furthermore, it should not be used if the model contains lagged versions of the dependent variable as independent variables. In such cases, Durbin’s h-test is a more appropriate alternative. By following these structured steps, researchers can ensure they are using the Durbin-Watson Table correctly and avoiding the common pitfalls associated with automated data analysis.

Finally, always document the results of the Durbin-Watson test in the methodology or results section of your research paper. Reporting the d statistic along with the critical values dL and dU provides transparency and allows readers to verify the reliability of your findings. This level of detail is a hallmark of high-quality academic and professional reporting in the field of statistics.

Limitations and Alternatives to the Durbin-Watson Test

While the Durbin-Watson Table is a foundational tool, it is not without its limitations. One of the most notable drawbacks is the aforementioned “inconclusive region.” When the test statistic falls between dL and dU, the researcher is left in a state of statistical limbo, unable to definitively prove or disprove the existence of autocorrelation. In such instances, more modern and robust tests, such as the Breusch-Godfrey test, are often preferred because they can test for higher-order serial correlation and do not suffer from the same inconclusive results.

Another limitation is that the Durbin-Watson test is specifically designed for first-order autocorrelation (AR(1)). It may fail to detect more complex patterns of correlation, such as seasonal effects or higher-order lags (AR(2), AR(3), etc.). For datasets where seasonality is a concern—such as monthly retail sales—the Durbin-Watson Table may provide a clean bill of health while significant correlation remains hidden in higher-order lags. Analysts must therefore use their domain expertise to decide if the first-order test is sufficient for their specific regression analysis.

Despite these limitations, the Durbin-Watson Table remains a staple of introductory and intermediate econometrics. Its simplicity and ease of interpretation make it an excellent first-line diagnostic. Even when more advanced tests are used, the Durbin-Watson statistic is often reported as a standard metric of model health. Understanding how to navigate the table and interpret its critical values is a fundamental skill for anyone serious about data science and statistical modeling, ensuring that the insights derived from data are both accurate and defensible.

Cite this article

stats writer (2026). How to Use the Durbin-Watson Table to Detect Autocorrelation. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/what-is-the-durbin-watson-table-and-how-is-it-used/

stats writer. "How to Use the Durbin-Watson Table to Detect Autocorrelation." PSYCHOLOGICAL SCALES, 1 Mar. 2026, https://scales.arabpsychology.com/stats/what-is-the-durbin-watson-table-and-how-is-it-used/.

stats writer. "How to Use the Durbin-Watson Table to Detect Autocorrelation." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/what-is-the-durbin-watson-table-and-how-is-it-used/.

stats writer (2026) 'How to Use the Durbin-Watson Table to Detect Autocorrelation', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/what-is-the-durbin-watson-table-and-how-is-it-used/.

[1] stats writer, "How to Use the Durbin-Watson Table to Detect Autocorrelation," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Use the Durbin-Watson Table to Detect Autocorrelation. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.