Table of Contents

A Chow Test in Python can be performed using the statsmodels package. This package contains the chow_test function, which takes parameters such as a regression model, the exogenous and endogenous variables, and the time periods to be tested. This function then returns the Chow Test statistic and the associated p-value, which indicate whether the coefficients of the regression model for the two time periods are statistically different.

A is used to test whether the coefficients in two different regression models on different datasets are equal.

This test is typically used in the field of econometrics with time series data to determine if there is a structural break in the data at some point.

The following a step-by-step example shows how to perform a Chow test in Python.

Step 1: Create the Data

First, we’ll create some fake data:

import pandas as pd #create DataFrame df = pd.DataFrame({'x': [1, 1, 2, 3, 4, 4, 5, 5, 6, 7, 7, 8, 8, 9, 10, 10, 11, 12, 12, 13, 14, 15, 15, 16, 17, 18, 18, 19, 20, 20], 'y': [3, 5, 6, 10, 13, 15, 17, 14, 20, 23, 25, 27, 30, 30, 31, 33, 32, 32, 30, 32, 34, 34, 37, 35, 34, 36, 34, 37, 38, 36]}) #view first five rows of DataFrame df.head() x y 0 1 3 1 1 5 2 2 6 3 3 10 4 4 13

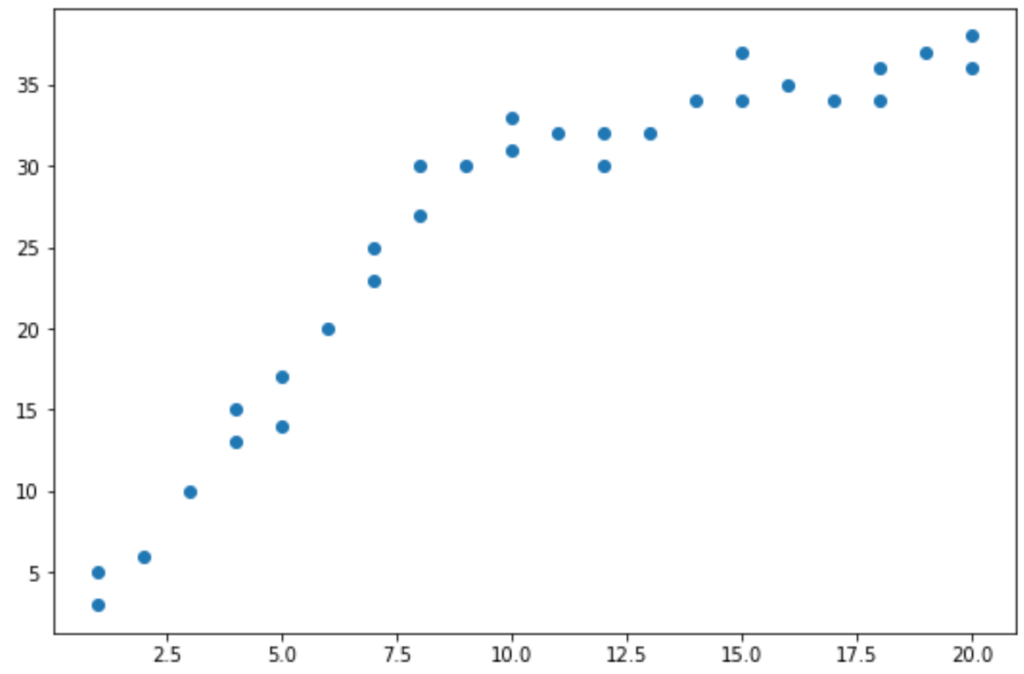

Step 2: Visualize the Data

Next, we’ll create a simple to visualize the data:

import matplotlib.pyplot as plt

#create scatterplot

plt.plot(df.x, df.y, 'o')

From the scatterplot we can see that the pattern in the data appears to change at x = 10.

Thus, we can perform the Chow test to determine if there is a structural break point in the data at x = 10.

Step 3: Perform the Chow Test

We can use the chowtest function from the package in Python to perform a Chow test.

First, we need to install this package using pip:

pip install chowtest

Next, we can use the following syntax to perform the Chow test:

from chow_test import chowtest chowtest(y=df[['y']], X=df[['x']], last_index_in_model_1=15, first_index_in_model_2=16, significance_level=.05) *********************************************************************************** Reject the null hypothesis of equality of regression coefficients in the 2 periods. *********************************************************************************** Chow Statistic: 118.14097335479373 p value: 0.0 *********************************************************************************** (118.14097335479373, 1.1102230246251565e-16)

Here’s what the individual arguments mean in the chowtest() function:

- y: The response variable in the DataFrame

- x: The predictor variable in the DataFrame

- last_index_in_model_1: The index value for the last point before the structural break

- first_index_in_model_2: The index value for the first point after the structural break

- significance_level: The significance level to use for the hypothesis test

From the output of the test we can see:

- F test statistic: 118.14

- p-value: <.0000

Since the p-value is less than .05, we can reject the null hypothesis of the test. This means we have sufficient evidence to say that a structural break point is present in the data.

In other words, two regression lines can fit the pattern in the data more effectively than a single regression line.

The following tutorials explain how to perform other common tests in Python:

Cite this article

stats writer (2025). How to Perform a Chow Test in Python Using Statsmodels. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-can-i-perform-a-chow-test-in-python/

stats writer. "How to Perform a Chow Test in Python Using Statsmodels." PSYCHOLOGICAL SCALES, 2 Dec. 2025, https://scales.arabpsychology.com/stats/how-can-i-perform-a-chow-test-in-python/.

stats writer. "How to Perform a Chow Test in Python Using Statsmodels." PSYCHOLOGICAL SCALES, 2025. https://scales.arabpsychology.com/stats/how-can-i-perform-a-chow-test-in-python/.

stats writer (2025) 'How to Perform a Chow Test in Python Using Statsmodels', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-can-i-perform-a-chow-test-in-python/.

[1] stats writer, "How to Perform a Chow Test in Python Using Statsmodels," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, December, 2025.

stats writer. How to Perform a Chow Test in Python Using Statsmodels. PSYCHOLOGICAL SCALES. 2025;vol(issue):pages.