Table of Contents

Introduction to Statistical Modeling and the R Environment

In the contemporary landscape of data analysis, the ability to accurately model empirical observations using theoretical distributions is a cornerstone of rigorous scientific inquiry. R, a premier statistical programming language, has established itself as the industry standard for such tasks due to its vast ecosystem of packages and robust computational capabilities. Among the various distributions utilized by statisticians, the Gamma distribution stands out as an exceptionally flexible tool for representing continuous, non-negative variables that exhibit a positive skew. This tutorial delves into the systematic process of fitting this distribution to a dataset, ensuring that researchers can derive meaningful parameters from their observations.

The utility of R lies not only in its core functionality but also in its extensible nature through the CRAN repository. Historically, the “MASS” package and its “fitdistr” function were the primary means of performing distribution fitting; however, modern workflows often favor the “fitdistrplus” package for its enhanced diagnostic tools and user-friendly interface. By mastering these tools, practitioners can move beyond simple descriptive statistics and venture into the realm of predictive modeling and statistical inference. Whether you are analyzing wait times in a queue, rainfall intensity, or insurance claim sizes, fitting a Gamma distribution provides a structured framework for understanding the underlying stochastic processes of your data.

Before proceeding with the technical implementation, it is vital to understand why the Gamma distribution is chosen over other models such as the normal distribution. While the normal distribution assumes symmetry and allows for negative values, many real-world phenomena are strictly positive and possess a “long tail” to the right. The Gamma distribution accommodates these characteristics through its shape and rate parameters, making it a more realistic choice for physical and financial data. This guide provides a comprehensive walkthrough, from data generation and package installation to the interpretation of complex diagnostic plots, ensuring a high level of detail for both novice and experienced users.

Theoretical Foundations of the Gamma Distribution

The Gamma distribution is defined by two primary parameters: the shape (often denoted as alpha) and the rate or scale (often denoted as beta). The probability density function of the Gamma distribution is mathematically designed to handle data that starts at zero and extends to infinity. The shape parameter determines the basic profile of the distribution; for instance, when the shape is equal to one, the Gamma distribution simplifies to an exponential distribution. As the shape parameter increases, the distribution becomes more “mound-shaped” and eventually approaches a normal distribution, demonstrating its incredible versatility in fitting various data profiles.

Understanding the interplay between these parameters is crucial for successful statistical model fitting. The rate parameter is the inverse of the scale parameter, and it controls the spread or “stretch” of the distribution. In R, functions like “rgamma” allow users to specify either the rate or the scale, providing flexibility depending on the specific conventions of the field of study. When we fit a distribution to a dataset, our objective is to find the specific values of shape and rate that maximize the likelihood of observing our particular set of data points, a process known as maximum likelihood estimation.

Moreover, the Gamma distribution is frequently used in Bayesian inference as a conjugate prior for various likelihood functions. Its mathematical properties allow for relatively straightforward calculations of the mean and variance, which are functions of the shape and rate parameters. By fitting this distribution, researchers gain the ability to calculate probabilities for future events, such as the likelihood of a variable exceeding a certain threshold. This theoretical depth is what makes the Gamma distribution an indispensable asset in the toolkit of any serious data scientist or statistician working within the R environment.

Synthesizing Sample Data for Distribution Analysis

To demonstrate the fitting process effectively, we must first work with a controlled dataset where the underlying parameters are known. In this tutorial, we generate a synthetic dataset named “z” by simulating values from a Gamma distribution and introducing a small amount of Gaussian noise. This approach mimics real-world scenarios where data rarely follows a theoretical distribution perfectly due to measurement errors or environmental factors. By using the “rgamma” function, we can create a sample size of 50 observations with a predefined shape parameter of 3 and a rate parameter of 10, providing a clear baseline for our statistical model.

The addition of noise is achieved through the “rnorm” function, which generates values from a normal distribution. In this instance, we use a mean of 0 and a very small standard deviation of 0.02. This ensures that while the primary structure of the data remains Gamma-distributed, it possesses the slight irregularities typical of empirical data analysis. Examining the first few values of this dataset using the “head” function allows us to verify that the data is continuous and positive, satisfying the basic requirements for Gamma fitting. The code snippet below illustrates this initialization process:

#generate 50 random values that follow a gamma distribution with shape parameter = 3 #and shape parameter = 10 combined with some gaussian noise z <- rgamma(50, 3, 10) + rnorm(50, 0, .02) #view first 6 values head(z) [1] 0.07730 0.02495 0.12788 0.15011 0.08839 0.09941

Once the data is generated, it is important to visualize the raw observations before applying any fitting algorithms. In a professional workflow, one might use a histogram or a density plot to observe the skewness and the range of the data. This preliminary exploratory data analysis helps in confirming that the Gamma distribution is indeed an appropriate candidate for the model. If the data contained negative values or was perfectly symmetrical, alternative distributions would need to be considered. This synthetic data generation serves as a pedagogical bridge between abstract theory and practical application.

Installing and Loading the fitdistrplus Package

While base R provides some capabilities for distribution fitting, the “fitdistrplus” package offers a much more comprehensive and specialized set of functions designed for this exact purpose. To utilize this package, it must first be installed from the CRAN repository using the “install.packages” command. This package is highly regarded for its ability to handle different types of data, including censored data, and for providing multiple estimation methods beyond just maximum likelihood estimation. Once installed, the library must be loaded into the current R session to make its functions accessible.

The “fitdistrplus” library is particularly useful because it standardizes the workflow for fitting any probability distribution. Whether you are fitting a Weibull, Lognormal, or Gamma distribution, the syntax remains consistent, which reduces the learning curve for researchers. Furthermore, the package integrates seamlessly with ggplot2 and other visualization libraries, allowing for high-quality publication-ready graphics. The following commands ensure that your environment is properly configured to begin the fitting process:

#install 'fitdistrplus' package if not already installed

install.packages('fitdistrplus')

#load package

library(fitdistrplus)After loading the package, it is often helpful to consult the documentation using the “help(package = ‘fitdistrplus’)” command. This provides detailed information on the various functions available, such as “descdist” for descriptive statistics and “bootdist” for bootstrapping the fitted parameters. The package authors have designed the software to assist users in the entire process of distribution fitting, from choosing the candidate distribution to validating the final statistical model. Ensuring that you are using the latest version of the package from CRAN is a best practice to benefit from the most recent bug fixes and performance improvements.

Executing the Maximum Likelihood Estimation

The core of the fitting process involves the “fitdist” function, which serves as the primary engine for parameter estimation within the “fitdistrplus” package. The general syntax for this function requires the dataset, the name of the distribution to be fitted (in this case, “gamma”), and the estimation method. While several methods exist—such as the method of moments or the maximum goodness-of-fit estimation—maximum likelihood estimation (MLE) is the most widely used due to its desirable asymptotic properties, such as unbiasedness and efficiency as the sample size grows.

When executing “fitdist” for a Gamma distribution, the function iteratively searches for the shape and rate parameters that maximize the log-likelihood function. This is a computational optimization problem that R handles efficiently in the background. It is important to note that the data must be strictly positive for the Gamma fitting to succeed; if the dataset contains zeros or negative numbers, the function will return an error, as the probability density function for Gamma is not defined for those values. The implementation is shown below:

#fit our dataset to a gamma distribution using mle fit <- fitdist(z, distr = "gamma", method = "mle") #view the summary of the fit summary(fit)

The resulting “fit” object is a S3 class that contains a wealth of information regarding the estimation results. By calling the “summary” function on this object, we can view the estimated parameters alongside their standard error. These errors provide a measure of the precision of our estimates; smaller standard errors indicate that our estimated parameters are likely very close to the true population parameters. This step is essential for data analysis, as it allows the researcher to quantify the uncertainty inherent in the modeling process.

Interpreting the Statistical Summary and Output

Upon running the “summary(fit)” command, R generates a detailed report that includes the estimated shape and rate parameters, the log-likelihood value, and information criteria such as the Akaike Information Criterion (AIC) and the Bayesian Information Criterion (BIC). These criteria are instrumental in model selection; for example, if you were comparing a Gamma fit against a Lognormal fit, the model with the lower AIC would generally be considered the better fit for the data. This quantitative approach removes much of the subjectivity from distribution fitting.

In addition to the point estimates, the summary provides a correlation matrix of the estimated parameters. This matrix reveals how changes in the shape parameter might correlate with changes in the rate parameter within the estimation process. High correlation can sometimes indicate that the model is overparameterized or that the parameters are difficult to distinguish given the current dataset. However, in the case of the Gamma distribution, these values are typically well-behaved provided the sample size is sufficient. The following image represents a typical output from the summary function:

A critical component of the summary is the standard error associated with each parameter. By dividing the estimate by its standard error, one can calculate a Z-score and determine if the parameters are significantly different from zero, although in the context of Gamma distributions, shape and rate must always be positive. The log-likelihood value itself is also useful for performing likelihood-ratio tests if one wishes to compare nested models. This level of detail ensures that the statistical model is not just a black box but a transparent representation of the data’s structure.

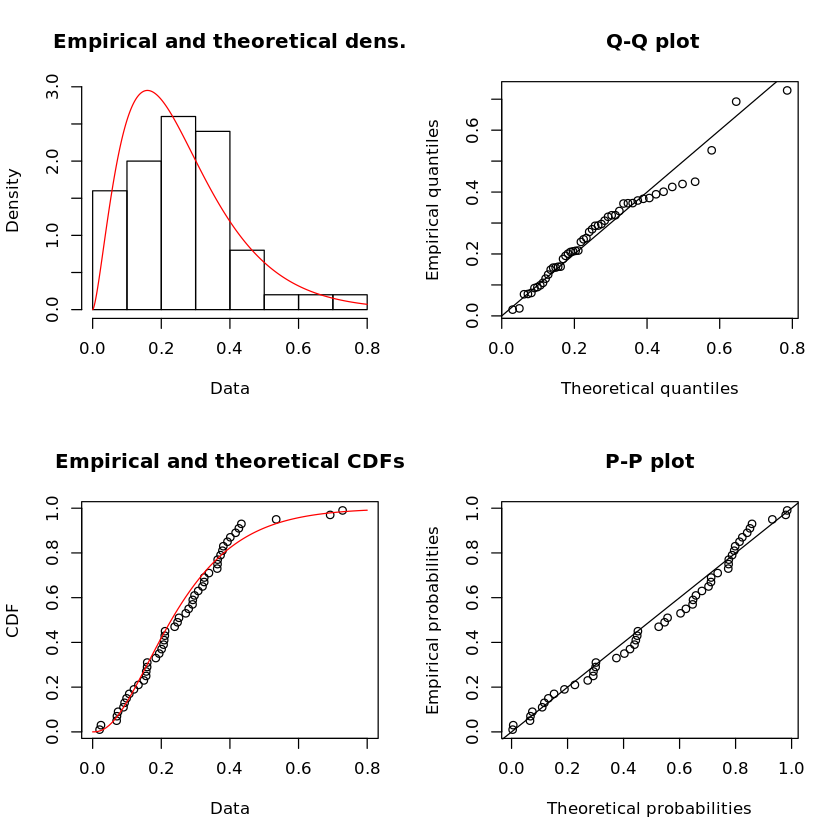

Visualizing the Goodness of Fit

While numerical summaries are vital, visual diagnostics are often more intuitive for assessing how well a distribution fits the data. The “fitdistrplus” package provides a powerful “plot” method that automatically generates four distinct charts: a histogram with the fitted density curve, a Q-Q plot, a P-P plot, and a comparison of the empirical and theoretical cumulative distribution functions (CDFs). Each of these plots offers a unique perspective on the goodness of fit and helps identify where the model may be deviating from the actual data.

The Q-Q plot (Quantile-Quantile plot) is particularly useful for checking the tails of the distribution. If the data points fall along the 45-degree reference line, it indicates that the theoretical quantiles match the empirical quantiles. Similarly, the P-P plot (Probability-Probability plot) evaluates the fit in the middle of the distribution. Discrepancies in these plots can signal that the Gamma distribution might not be the optimal choice, perhaps suggesting that a heavier-tailed distribution is required. To generate these visualizations, use the following syntax:

#produce plots plot(fit)

The resulting graphical output, shown below, provides a holistic view of the model’s performance. The “Empirical and theoretical densities” plot allows for a direct comparison between the frequency of the data and the probability density function of the fitted Gamma model. If the curve aligns well with the peaks and spread of the histogram, the researcher can have higher confidence in the model’s validity. These visualizations are essential for communicating results to stakeholders who may not be familiar with the underlying maximum likelihood estimation mathematics.

Comprehensive Code Implementation for Gamma Fitting

To facilitate reproducibility and clarity, it is beneficial to consolidate the individual steps into a single, cohesive script. This allows for easy modification of parameters, such as changing the sample size or adjusting the noise level, to see how the statistical model responds. In a professional data analysis environment, such scripts are often version-controlled and shared among team members to ensure consistency in methodology. The complete workflow for fitting a Gamma distribution in R is presented here:

#install 'fitdistrplus' package if not already installed

install.packages('fitdistrplus')

#load package

library(fitdistrplus)

#generate 50 random values that follow a gamma distribution with shape parameter = 3

#and shape parameter = 10 combined with some gaussian noise

z <- rgamma(50, 3, 10) + rnorm(50, 0, .02)

#fit our dataset to a gamma distribution using mle

fit <- fitdist(z, distr = "gamma", method = "mle")

#view the summary of the fit

summary(fit)

#produce plots to visualize the fit

plot(fit)

In addition to the code provided, users might consider exploring the “gofstat” function within the “fitdistrplus” package. This function provides formal goodness of fit statistics, such as the Kolmogorov-Smirnov test, the Cramer-von Mises test, and the Anderson-Darling test. These tests provide p-values that can formally test the null hypothesis that the data follows a Gamma distribution. While visual inspection is important, these formal tests add another layer of statistical rigor to your findings.

Ultimately, using R to fit a Gamma distribution enables a deeper understanding of positively skewed data. By identifying the specific shape and rate that define your dataset, you can perform simulations, calculate risk metrics, and make informed decisions based on the underlying probability structure. This tutorial serves as a robust foundation for anyone looking to apply advanced distributional modeling to their own unique datasets, leveraging the full power of the statistical programming language ecosystem.

Cite this article

stats writer (2026). How to Fit a Gamma Distribution to Your Data in R. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/how-can-i-use-r-to-fit-a-gamma-distribution-to-a-dataset/

stats writer. "How to Fit a Gamma Distribution to Your Data in R." PSYCHOLOGICAL SCALES, 2 Mar. 2026, https://scales.arabpsychology.com/stats/how-can-i-use-r-to-fit-a-gamma-distribution-to-a-dataset/.

stats writer. "How to Fit a Gamma Distribution to Your Data in R." PSYCHOLOGICAL SCALES, 2026. https://scales.arabpsychology.com/stats/how-can-i-use-r-to-fit-a-gamma-distribution-to-a-dataset/.

stats writer (2026) 'How to Fit a Gamma Distribution to Your Data in R', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/how-can-i-use-r-to-fit-a-gamma-distribution-to-a-dataset/.

[1] stats writer, "How to Fit a Gamma Distribution to Your Data in R," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, March, 2026.

stats writer. How to Fit a Gamma Distribution to Your Data in R. PSYCHOLOGICAL SCALES. 2026;vol(issue):pages.