Table of Contents

Introduction to the Standard Error of the Estimate

The standard error of the estimate is one of the most fundamental metrics used to evaluate the accuracy and precision of a statistical regression model. At its core, it provides a crucial measure of the average distance that the observed data points fall from the regression line, which serves as the predicted relationship between the variables. This metric is indispensable for statisticians and analysts, as it quantifies the variability, or scatter, of the data around the best-fit line, thereby reflecting the model’s predictive reliability. A robust understanding of the standard error of the estimate is essential when determining whether a regression equation is suitable for making reliable forecasts or inferences about a population.

Unlike the standard deviation of the dependent variable, which measures total variability, the standard error of the estimate specifically isolates the variability that remains unexplained by the independent variables included in the model. It is, therefore, a measure of the typical size of the model’s residuals—the vertical distances between the actual data points and the estimated regression line. When building a regression model, the primary goal is often to minimize this error, ensuring that the line closely approximates the true underlying relationship in the data.

This powerful statistical tool is conventionally denoted as σest (sigma sub est) or sometimes as se in sample notation. Its interpretation is straightforward: a smaller value indicates that the data points are tightly clustered around the regression line, suggesting a highly accurate predictive model where the independent variables account for a large proportion of the variance in the dependent variable. Conversely, a large standard error of the estimate signals significant scatter, implying that the model is a poor fit for the data and that predictions based on this line will carry a higher degree of uncertainty. This metric serves as a foundational step in assessing overall model fitness before proceeding to more complex hypothesis testing or prediction intervals.

The Mathematical Foundation: Formula and Components

The calculation of the standard error of the estimate derives directly from the fundamental concept of minimizing the squared errors, which is the basis for the ordinary least squares (OLS) method used in linear regression. The formula essentially calculates the root mean square of the residuals, providing an average measure of the deviation. While in introductory contexts the formula is often simplified for descriptive purposes, it is represented as the square root of the sum of the squared differences between the actual and predicted values, divided by the number of observations.

The simplified formula commonly encountered for descriptive purposes is presented below:

σest = √Σ(y – ŷ)2/n

Understanding the components within this mathematical expression is key to appreciating its statistical meaning. The term y represents the observed value of the dependent variable for a given observation—the actual data point recorded. The symbol ŷ (read as “y-hat”) represents the predicted value generated by the regression equation for that same observation. The difference (y – ŷ) is known as the residual, which measures the error of prediction for that specific data point. By squaring this residual, we ensure that positive and negative errors do not cancel each other out, and we penalize larger errors more heavily, consistent with the OLS principle.

The variables used in the calculation are defined as follows:

- y: The observed value of the dependent variable.

- ŷ: The predicted value derived from the regression line.

- n: The total number of observations in the dataset.

Interpreting the Standard Error (σest)

The interpretation of the standard error of the estimate is critical for evaluating the performance of a regression model. Unlike correlation coefficients or R-squared values, which are unitless or scaled between 0 and 1, the standard error is expressed in the same units as the dependent variable. This inherent characteristic makes it highly practical, as it provides a direct, intuitive measure of prediction accuracy: if the dependent variable is measured in kilograms, the standard error is also measured in kilograms, representing the typical prediction error in those units.

The primary rule of interpretation centers on the magnitude of the calculated value. The standard error of the estimate fundamentally gives us an idea of how well a regression model fits a dataset, with the implications summarized concisely:

- The smaller the value, the better the fit. A low σest means the model’s predictions are very close to the actual observations.

- The larger the value, the worse the fit. A high σest indicates significant variability, suggesting the regression line is not a strong predictor.

Consider two regression models developed to predict housing prices. If Model A has a standard error of the estimate of $5,000, and Model B has an error of $50,000, Model A is clearly superior because its predictions are significantly more precise. Therefore, the standard error acts as a crucial benchmark for comparing the predictive power of different models applied to the same dataset or similar types of data. It serves as a necessary reality check on the model’s practical utility, ensuring that the precision meets the requirements of the analytical task at hand.

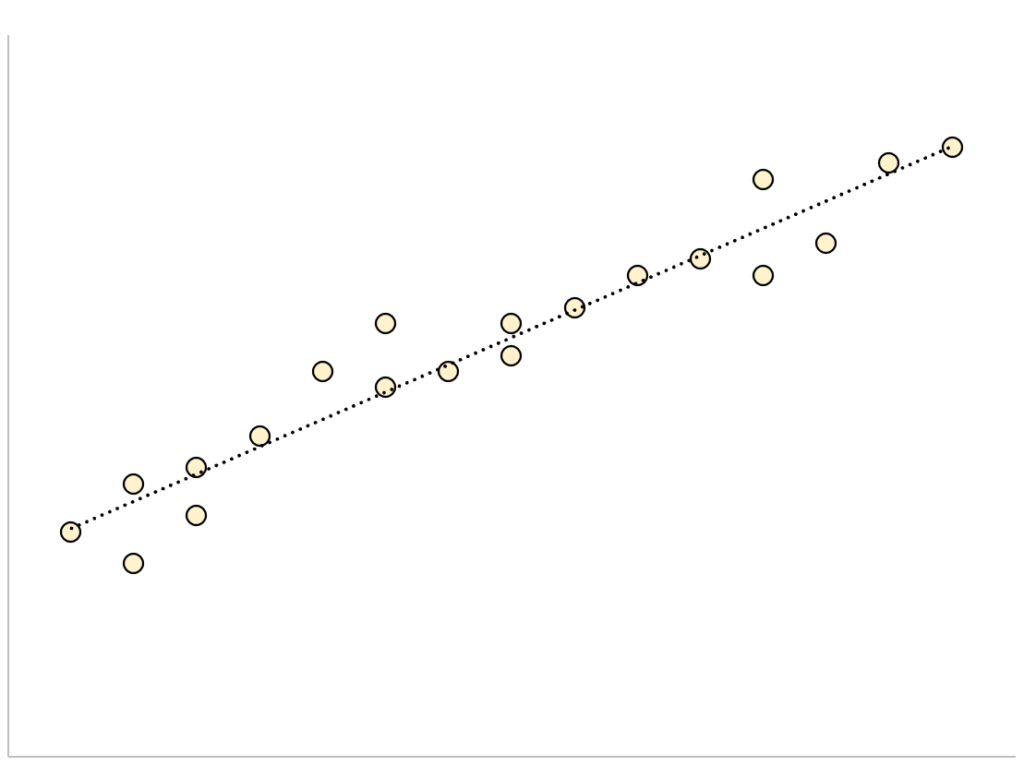

Visualizing the Fit: Close vs. Loose Data Scatter

The standard error of the estimate has a compelling visual representation that clarifies its role in model assessment. It directly relates to how closely the cloud of data points hugs the estimated regression line. This visual check is often the first qualitative step in evaluating a regression analysis before diving into quantitative metrics and confirms the numerical result.

For a regression model that achieves a small standard error of the estimate, the scatter plot will distinctly show the data points closely packed around the estimated regression line. This tight clustering signifies high precision; the vertical distances (the residuals) between the observed values and the line are generally small. When interpreting such a plot, an analyst can be confident that the independent variable(s) successfully explain the variation in the dependent variable, resulting in minimal prediction error. This ideal scenario is depicted below, illustrating a strong fit:

Conversely, for a regression model that yields a large standard error of the estimate, the visual representation is starkly different. The data points will be more loosely scattered, spreading widely both above and below the regression line. This considerable dispersion indicates substantial unexplained variance, meaning the residuals are large on average.

When the scatter is loose, as shown in the subsequent image, the model possesses low predictive power. Although the regression line still represents the “best fit” based on the OLS criteria, the large standard error warns that predictions based on this line are subject to high uncertainty. A high standard error often prompts analysts to consider adding more relevant explanatory variables to the model or exploring non-linear relationships that might better capture the underlying patterns in the data:

Practical Application: Calculating σest in Excel

Following the theoretical exploration of the standard error of the estimate, it is valuable to apply these concepts using a practical example. The subsequent steps demonstrate the straightforward process of calculating and interpreting the standard error of the estimate for a simple linear regression model utilizing Microsoft Excel’s built-in statistical analysis tools. This concrete example will solidify the understanding of where this critical metric appears in standard statistical software output.

We will use a small dataset relating two variables, X and Y, to demonstrate the process. While advanced statistical packages offer more detailed output, Excel provides an accessible and rapid method for obtaining the necessary regression diagnostics.

The following example shows how to calculate and interpret the standard error of the estimate for a regression model in Excel.

Step-by-Step Data Preparation in Excel

The initial and most crucial phase of any regression analysis is the proper structuring and input of the data. For this example, we begin by entering the paired values for the independent variable (X) and the dependent variable (Y) into separate columns within an Excel worksheet. Ensuring data accuracy at this stage is paramount, as errors here will propagate throughout the subsequent analysis and skew the standard error calculation.

First, enter the values for the dataset into the spreadsheet, typically with the independent variable in the left column and the dependent variable in the adjacent column, as shown in the following image:

Once the data is accurately entered, we utilize Excel’s powerful analysis features. The primary tool needed for this regression analysis is the Data Analysis ToolPak, an add-in that must be activated if it is not already visible in the ribbon interface. Assuming the ToolPak is active, proceed to access the regression function.

Generating Regression Output using Data Analysis ToolPak

To initiate the regression analysis and calculate the necessary statistics, navigate through the Excel interface. First, click the Data tab located along the top ribbon interface. Following this, locate and click the Data Analysis option, typically found within the Analyze group, which opens the dialog box for selecting statistical procedures.

If you don’t see this option, you need to first install the Analysis ToolPak add-in via Excel Options. In the new window that appears after clicking Data Analysis, scroll down the list of available tools, click on Regression, and then confirm the selection by clicking OK. This action prepares the system to accept the input ranges for the analysis.

In the new Regression window that appears, fill in the following information, specifying the input ranges for Y and X. Ensure the dependent variable is entered in the Y Range and the independent variable in the X Range. We will also check the option for Labels if the data includes headers and specify a suitable output range for the results.

Once you click OK, the comprehensive regression output will appear, containing all the calculated statistics derived from the least squares method, including the key metric we seek.

Interpreting the Excel Output and Regression Equation

The resulting regression output sheet contains the necessary metrics for model evaluation. We must locate the Standard Error within the Regression Statistics summary table. This value is the calculated standard error of the estimate for our model.

From the output, we can observe that the standard error of the estimate for this regression model turns out to be 6.006. In simple terms, this tells us that the average data point falls 6.006 units from the regression line. This value is used directly to assess the model’s precision in predicting the dependent variable.

We can also use the coefficients from the regression table (the Intercept and X Variable 1 coefficient) to construct the estimated regression equation:

ŷ = 13.367 + 1.693(x)

This equation provides the predicted point, but it is the standard error of 6.006 that provides the context for the uncertainty surrounding that prediction. A smaller standard error would lead to more confidence in the predicted value, while a larger one suggests a higher expected deviation.

Using σest to Construct Confidence Intervals

One of the most powerful applications of the standard error of the estimate is its use in constructing confidence intervals. While the estimated regression equation provides a single point prediction (ŷ), the standard error allows us to quantify the uncertainty around that prediction, providing a range within which the true mean value of Y is likely to fall for a given X. This range is crucial for making informed decisions based on the statistical model.

We can use the estimated regression equation and the standard error of the estimate to construct a 95% confidence interval for the predicted value of a certain data point. For large samples and normally distributed errors, the 95% interval is commonly approximated using the critical Z-score of 1.96.

For example, suppose the independent variable x is equal to 10. Using the estimated regression equation, we would predict that y would be equal to:

ŷ = 13.367 + 1.693*(10) = 30.297

And we can obtain the 95% confidence interval for this estimate by using the following formula:

- 95% C.I. = [ŷ – 1.96 * σest, ŷ + 1.96 * σest]

For our example, the 95% confidence interval would be calculated as:

- 95% C.I. = [30.297 – 1.96*6.006, 30.297 + 1.96*6.006]

- 95% C.I. = [30.297 – 11.772, 30.297 + 11.772]

- 95% C.I. = [18.525, 42.069]

This final calculated interval demonstrates that we are 95% confident that the true average value of Y, when X is 10, lies between 18.525 and 42.069. The standard error of the estimate is therefore integral to providing the bounds of certainty for any regression prediction.

Cite this article

stats writer (2025). How to Calculate the Standard Error of the Estimate. PSYCHOLOGICAL SCALES. Retrieved from https://scales.arabpsychology.com/stats/what-is-the-standard-error-of-the-estimate/

stats writer. "How to Calculate the Standard Error of the Estimate." PSYCHOLOGICAL SCALES, 6 Dec. 2025, https://scales.arabpsychology.com/stats/what-is-the-standard-error-of-the-estimate/.

stats writer. "How to Calculate the Standard Error of the Estimate." PSYCHOLOGICAL SCALES, 2025. https://scales.arabpsychology.com/stats/what-is-the-standard-error-of-the-estimate/.

stats writer (2025) 'How to Calculate the Standard Error of the Estimate', PSYCHOLOGICAL SCALES. Available at: https://scales.arabpsychology.com/stats/what-is-the-standard-error-of-the-estimate/.

[1] stats writer, "How to Calculate the Standard Error of the Estimate," PSYCHOLOGICAL SCALES, vol. X, no. Y, ص Z-Z, December, 2025.

stats writer. How to Calculate the Standard Error of the Estimate. PSYCHOLOGICAL SCALES. 2025;vol(issue):pages.